Beacon Hill condos for sale: The importance of your credit score

Boston Condos for Sale and Apartments for Rent

Beacon Hill condos for sale: The importance of your credit score

Your credit score plays a big role in buying a Boston Beacon Hill condo for sale purchasing process. It’s one of the key factors lenders look at to determine which loan options you qualify for and what your terms might be. But there’s a myth about credit scores that may be holding some buyers back.

The Myth: You Need To Have Perfect Credit

According to Fannie Mae, only 32% of potential homebuyers have a good idea of what credit score lenders actually require.

That means two-thirds of condo buyers don’t actually know what lenders are looking for – and most overestimate the minimum credit score needed.

The Reality: Perfect Isn’t Necessary

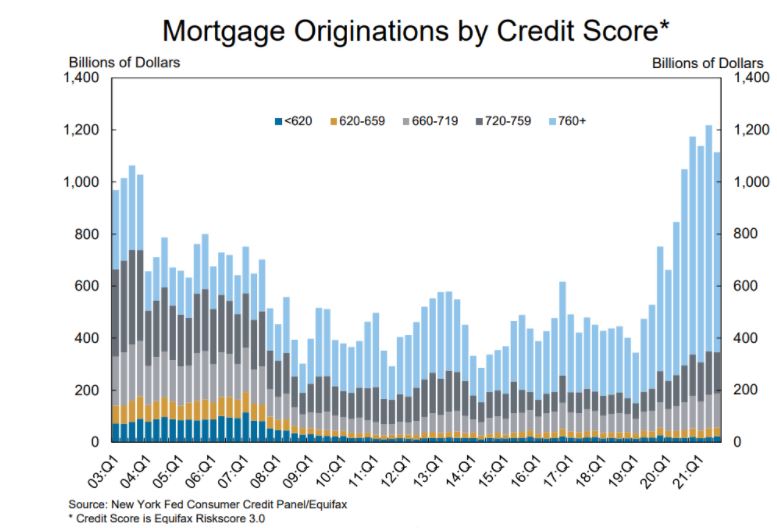

But the truth is, you don’t need perfect credit to become a homeowner. To see the average score, by loan type, for recent homebuyers check out the graph below:

There is no set cut-off score across the board. As FICO explains:

There is no set cut-off score across the board. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders, and there are many additional factors that lenders may use . . .”

So, even if your credit score isn’t as high as you’d like, you may still be able to get a home loan. Just know that, even though you don’t need perfect credit to buy a home, your score can have an impact on your loan options and the terms you’re able to get.

Work with a trusted lender who can walk you through what you’d qualify for.

Simple Tips To Improve Your Credit Score

If you want to open up your options a bit more after talking to a lender, here are a few tips from Experian and Freddie Mac that can help give your score a boost:

1. Pay Your Bills on Time

This includes everything from credit cards to utilities and other monthly payments. A track record of on-time payments shows lenders you’re responsible and reliable.

2. Pay Down Outstanding Debt

Reducing your overall debt not only improves your credit utilization ratio (how much credit you’re using compared to your total limit) but also makes you a lower-risk borrower in the eyes of lenders. That makes them more likely to approve a loan with better terms.

3. Hold Off on Applying for New Credit

While opening new credit accounts might seem like a quick way to boost your score, too many applications in a short period can have the opposite effect. Focus on improving your existing accounts instead.

Beacon Hill Condo for Sale and the Bottom Line

Your credit score doesn’t have to be perfect to qualify for a home loan. The best way to know where you stand? Work with a trusted lender to explore your options.

_________________________________

Beacon Hill condos for sale: The importance of your credit score

If you want to buy a Boston Beacon Hill home, you should know your credit score is a critical piece of the puzzle when it comes to qualifying for a mortgage. Lenders review your credit to see if you typically make payments on time, pay back debts, and more. Your credit score can also help determine your mortgage rate. An article from US Bank explains:

“A credit score isn’t the only deciding factor on your mortgage application, but it’s a significant one. So, when you’re house shopping, it’s important to know where your credit stands and how to use it to get the best mortgage rate possible.”

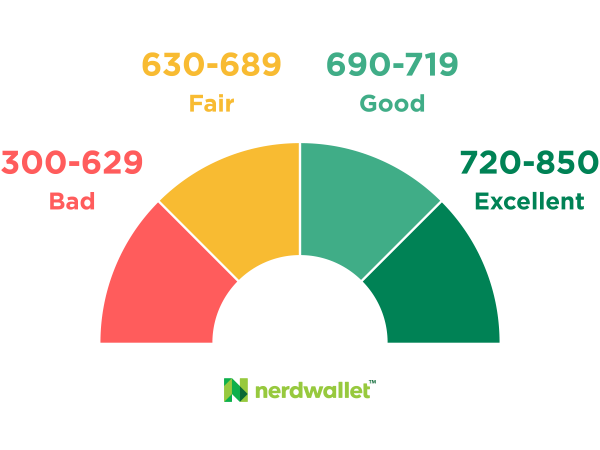

That means your credit score may feel even more important to your Boston Beacon Hill homebuying plans right now since mortgage rates are a key factor in affordability. According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. The same article from US Bank explains:

“Your credit score (commonly called a FICO Score) can range from 300 at the low end to 850 at the high end. A score of 740 or above is generally considered very good, but you don’t need that score or above to buy a home.”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate you’re able to get. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

- Your Payment History: Late payments can have a negative impact by dropping your score. Focus on making payments on time and paying any existing late charges quickly.

- Your Debt Amount (relative to your credit limits): When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible.

- Credit Applications: If you’re looking to buy something, don’t apply for additional credit. When you apply for new credit, it could result in a hard inquiry on your credit that drops your score. Finding ways to make your credit score better could help you get a lower mortgage rate. If you want to learn more, talk to a trusted lender.

Beacon Hill Condos and the Bottom Line

Byline – John Ford Boston Beacon Hill Condo Broker 137 Charles St. Boston, MA 02114

Call today!

Where is Ford Realty Located?

Ford Realty is located in 137 Charles Street in Beacon Hill

Byline – John Ford – Boston Seaport Condo Broker.

Where is Ford Realty Located?

Ford Realty is located in 137 Charles Street in Beacon Hill

++++++++++++

Beacon Hill condos for sale: The importance of your credit score

Boston Condos for Sale and Apartments for Rent

Credit Scores for Beacon Hill Condos: What You Need to Know for Financing

Beacon Hill condos for sale: The importance of your credit score

Securing the keys to your dream condo in Beacon Hill can invoke a surge of excitement. Yet, there’s one significant factor waiting in the shadows that could potentially dampen this thrill – your credit score. Designed to tie up potential loose ends, credit scores play a pivotal role in the home financing process. In fact, they could very well stand between you and your prime Beacon Hill abode. Want a smooth sail as you navigate through the complex corners of securing finance for luxury condos? Stick around as we unpack everything you need to know about credit scores for Beacon Hill condos, from understanding this financial cipher to strategies on boosting your numbers. The road to homeownership need not be rocky; get equipped today, avoid pitfalls tomorrow.

Credit scores can play a significant role in the homebuying process, including securing financing and determining interest rates. Having a good credit score can increase your chances of being approved for a mortgage and may result in lower interest rates and better loan terms. It’s important to monitor your credit report regularly to ensure accuracy and take steps to improve your credit score if necessary before applying for a mortgage to purchase a Beacon Hill condo.

Credit Score Essentials for Beacon Hill Condos

When it comes to purchasing a Beacon Hill condo, your credit score plays a crucial role in determining the financing options available to you. A credit score is a numerical representation of your creditworthiness, indicating how reliable you are at repaying borrowed funds. It provides lenders with a snapshot of your financial history and helps them assess the level of risk involved in lending to you. Understanding the essentials of credit scores will empower you in your quest to secure financing for your dream Beacon Hill condo.

Imagine you’ve found the perfect Beacon Hill condo that checks all the boxes – beautiful views, excellent amenities, and a prime location. Now it’s time to consider financing options. Your credit score becomes the gatekeeper, either granting you access to favorable loan terms or making it challenging to secure financing altogether.

Your credit score is calculated based on several factors such as payment history, credit utilization ratio, length of credit history, types of credit used, and recent applications for new credit. These factors contribute to your overall creditworthiness and impact your ability to obtain favorable interest rates and loan terms. Typically, lenders consider a higher credit score as an indication of less risk and may be more inclined to offer more favorable loan conditions.

For example, let’s say two individuals are looking to finance a Beacon Hill condo with similar financial circumstances but different credit scores. The person with a higher credit score may be offered a lower interest rate, resulting in tens of thousands of dollars saved over the life of the loan compared to someone with a lower credit score.

Now that we understand the importance of credit scores in securing financing, let’s explore the function they serve and how they can impact your options.

The Function of Credit Scores

In essence, credit scores serve as a measure of financial responsibility. They reflect an individual’s past behavior in managing their debts and provide lenders with insights into the likelihood of timely repayment. A high credit score indicates a good track record of responsible financial management, making lenders more confident in extending credit and offering better terms.

Lenders use credit scores to assess risk and determine whether to approve loan applications, what interest rates to offer, and what loan amounts are suitable. The higher your credit score, the more likely you are to be approved for financing and benefit from lower interest rates.

Think of your credit score as a reflection of your financial reputation. Just as a good reputation can open doors in various aspects of life, a high credit score can unlock opportunities for favorable financing terms.

It’s important to note that each lender may have specific criteria for determining loan eligibility based on credit scores. While some lenders may have stricter requirements, others may offer more flexible options tailored to individuals with lower credit scores. It’s always a good idea to explore multiple financing options and compare terms from different lenders to find the best fit for your unique situation.

For instance, if you have a lower credit score due to an isolated past financial setback or limited credit history, certain lenders may be willing to work with you by offering specialized loans or granting access to programs designed specifically for borrowers with less-than-perfect credit.

Understanding the function of credit scores empowers you to take control of your financial situation and improve your chances of securing favorable financing for your Beacon Hill condo.

Minimum Credit Score Exigencies

When it comes to financing a Beacon Hill condo, your credit score plays a vital role in determining your eligibility and the terms of your loan. While specific requirements may vary among lenders, there are certain minimum credit score exigencies that you should be aware of. These thresholds serve as benchmarks for lenders to assess the risk associated with lending to you.

To give you an idea, conventional loans typically require a minimum credit score of 620 to secure financing. However, keep in mind that higher scores can result in better interest rates and loan terms. Government-backed loans, such as those offered by the Federal Housing Administration (FHA), often have more lenient credit score requirements, with some lenders considering scores as low as 500.

It’s critical to note that these minimum credit score exigencies are only part of the equation. Lenders also consider other factors when evaluating your application.

Lender Specifications and Factors

Each lender has its own set of specifications and factors that they take into account when reviewing loan applications. Credit scores are just one piece of this puzzle. Apart from assessing your creditworthiness, lenders also consider several other aspects such as:

Employment History: Lenders look at your employment history to gauge your stability and financial capability to repay the loan.

Debt-to-Income Ratio (DTI): This ratio compares your monthly debt obligations to your monthly income. Lenders use this metric to determine if you have the financial capacity to handle additional debt.

Financial Reserves: Some lenders may want assurance that you have enough savings or investments in case unexpected expenses arise after purchasing a Beacon Hill condo.

Loan-to-Value Ratio (LTV): The LTV ratio measures the loan amount against the appraised value of the property. A lower LTV ratio demonstrates less risk for the lender.

While credit score is undeniably significant in securing financing for a Beacon Hill condo, lenders also take into account various other factors to assess your overall financial health and ability to repay the loan. Successfully meeting lender specifications and demonstrating positive factors can help strengthen your loan application and improve your chances of obtaining favorable terms.

Now that we have a good understanding of the minimum credit score exigencies and the lender specifications and factors, let’s explore the elements that influence credit scores themselves.

- According to real estate statistics, in 2023, the minimum credit score needed to secure a conventional mortgage loan in the United States is typically around 620.

- A survey by Experian in 2020 stated that Boston residents had an average credit score of 734, which is higher than the national average and indicates greater chances of approval for premium loan products.

- The National Association of Realtors reported in 2023 that about 30% of condo buyers in high-value areas like Beacon Hill are unable to secure a mortgage due to low credit scores.

- Apart from credit score, lenders consider several other factors such as employment history, debt-to-income ratio, financial reserves, and loan-to-value ratio when reviewing loan applications. Understanding these factors and meeting lender specifications can help improve your chances of securing favorable loan terms. Additionally, it is important to understand the elements that influence credit scores themselves.

Elements Influencing Credit Scores

When it comes to financing a Beacon Hill condo, your credit score plays a significant role in determining your eligibility and the terms of your loan. Understanding the various elements that influence credit scores can help you navigate this process more effectively. Let’s explore some of these key factors.

Payment History: Your payment history is one of the most critical components of your credit score. Lenders want to see a consistent track record of on-time payments for loans, credit cards, and other debts. Late payments or defaults can significantly impact your score negatively.

For instance, if you’ve missed multiple payments on previous student loans or have a history of delinquency with your credit cards, lenders may view you as a higher risk borrower.

Credit Utilization: Another vital element that lenders consider is your credit utilization ratio. This refers to the amount of credit you’re using compared to your total available credit limit. Ideally, you should aim to keep your credit utilization below 30%. Higher balances can indicate financial strain and may have a negative impact on your score.

Think of it like managing your expenses within a budget – maxing out all your available credit cards could signal financial strain and lead lenders to question your ability to handle additional debt responsibly.

Length of Credit History: The length of time you’ve had credit also affects your credit score. Having a longer credit history demonstrates stability and responsible borrowing behavior. It allows lenders to assess how you’ve managed loans and debt over an extended period.

For example, someone who has consistently paid their mortgage or car loan for ten years will likely have a more favorable credit score than someone who just started building their credit profile a few months ago.

Types of Credit: Lenders also consider the different types of credit accounts you have. A healthy mix of installment loans (such as a car loan) and revolving credit (like credit cards) can demonstrate your ability to manage various types of debt responsibly.

Having only one type of credit, or solely relying on credit cards without any installment loans, may negatively impact your score.

Recent Credit Inquiries: Every time you apply for new credit, such as a loan or credit card, a hard inquiry is made on your credit report. While it’s normal to have occasional inquiries, frequent or multiple applications within a short period can raise concerns for lenders. It may suggest financial instability or an intention to take on excessive debt.

By understanding these elements that influence your credit score, you can now turn your attention to evaluating your own financial circumstances and resources.

Financial Circumstances and Resources

Your financial circumstances and available resources also play a crucial role in the financing process for Beacon Hill condos. Lenders consider various aspects when assessing your ability to repay the loan and manage homeownership responsibilities. Let’s dive into some key factors related to financial circumstances and resources.

Income Stability: Lenders want to ensure that you have a stable income that is sufficient to cover mortgage payments and other living expenses. They will assess factors such as the consistency of your income source, job history, and monthly earnings. A higher income with a steady employment history provides reassurance to lenders.

For instance, if you’ve been working at the same company for several years and have received regular salary increases, it demonstrates stability and financial security.

Debt-to-Income Ratio: Your debt-to-income (DTI) ratio compares the amount of debt you owe each month to your gross monthly income. Lenders use this ratio to evaluate how much of your income goes towards debt repayment. Ideally, they prefer borrowers with a lower DTI ratio, as it indicates a smaller financial burden. A higher DTI ratio may raise concerns about your ability to afford additional debt.

For example, if your monthly debt payments (such as credit card bills, car loans, and student loans) total $2,000, and your gross monthly income is $6,000, your DTI ratio is 33%.

Your DTI ratio is an important metric for lenders because it helps them assess your ability to handle additional mortgage debt effectively without becoming financially strained.

Assets and Reserves: Lenders also consider the assets you own and the reserves you have available. These include savings accounts, investment portfolios, and other valuable assets. Having substantial assets can provide reassurance to lenders since they act as a safety net in case of unexpected expenses or financial difficulties.

For instance, if you have significant savings or investments that can cover several months’ worth of mortgage payments, it demonstrates that you are financially prepared for homeownership.

Creditworthiness of Co-Borrowers: In some cases, having a co-borrower with a strong credit history and stable income can positively impact your financing prospects. Lenders may consider their financial circumstances alongside yours when evaluating your loan application.

For example, if you’re applying for a loan together with a spouse who has an excellent credit score and high income, it can improve your overall borrowing capacity and increase the chances of loan approval.

By understanding how financial circumstances and resources influence the financing process for Beacon Hill condos, you can better position yourself for success in obtaining a loan. As you move forward in your journey to financing a condo in this vibrant neighborhood, keep these factors in mind to make informed decisions that align with your financial goals.

Qualification Procedures for Beacon Hill Loan

When considering financing options for Beacon Hill condos, it’s crucial to understand the qualification procedures involved. Lenders have specific criteria that applicants must meet to secure a loan. By familiarizing yourself with these procedures, you can better prepare and increase your chances of qualifying.

The first step in the qualification process is assessing your credit score. Lenders use credit scores as a measure of an individual’s creditworthiness. A higher credit score indicates a lower risk borrower, making it easier to qualify for a loan and potentially secure more favorable terms. On the other hand, a lower credit score may lead to more stringent requirements or even denial of a loan application.

Consider this scenario: Imagine you’re looking to purchase a beautiful condominium in Beacon Hill. You’ve saved up for the down payment and have steady income; however, your credit score is not as high as you’d like it to be due to some past financial challenges. To increase your chances of qualifying for the loan, you might consider taking steps to improve your credit score before applying, such as paying down existing debt and making all future payments on time.

Once you have assessed your credit score, lenders will also evaluate your income and debt-to-income ratio (DTI). Your income plays an essential role in determining whether you have sufficient funds to cover monthly mortgage payments. Lenders typically want to ensure that your housing expenses do not exceed a certain percentage of your gross monthly income.

In addition to income, lenders consider DTI, which compares your monthly debt obligations (including any existing loans or debts) with your gross monthly income. A lower DTI ratio demonstrates a borrower’s ability to manage their financial obligations effectively and may increase the likelihood of qualifying for a loan.

Think of qualification procedures for Beacon Hill loans like preparing for a job interview. Just as employers assess qualifications and skills to gauge an applicant’s suitability for a position, lenders evaluate credit scores, income, and DTI ratios to determine your eligibility for financing. By presenting yourself as a reliable candidate with a strong financial foundation, you enhance your chances of securing loan approval.

Once these factors have been considered, lenders may also evaluate other aspects such as employment history, the stability of your income source, and any outstanding legal judgments or bankruptcies. These additional criteria provide lenders with a more comprehensive picture of your financial situation and further contribute to their assessment of your loan application.

Understanding the qualification procedures for Beacon Hill loans is essential when seeking financing for a condo purchase. By familiarizing yourself with the requirements related to credit scores, income, DTI ratios, and other pertinent factors, you can take proactive steps to improve your chances of qualifying for a loan. Remember that each lender may have slightly different criteria, so it’s beneficial to research and compare options before settling on a specific lender.

Are there any exceptions or alternative financing options for individuals with lower credit scores?

Yes, there are exceptions and alternative financing options available for individuals with lower credit scores. One such option is FHA loans, which have more lenient credit score requirements compared to traditional mortgages. According to recent statistics, the average FICO score for FHA borrowers in 2021 was around 680, significantly lower than the average required by conventional lenders. Additionally, some specialized lenders and credit unions offer loans specifically designed for individuals with lower credit scores, providing them with an opportunity to qualify for financing despite their credit history.

What steps can be taken to improve credit scores prior to applying for a Beacon Hill condo loan?

To improve credit scores before applying for a Beacon Hill condo loan, there are a few steps one can take. Firstly, it is important to pay bills on time and avoid late payments, as payment history accounts for 35% of your credit score. Secondly, reducing credit card balances and keeping credit utilization below 30% can positively impact your score. Additionally, checking and disputing any errors on your credit report is crucial. According to Experian, the average credit score in the United States is 710, so taking these steps can help increase your chances of securing a favorable condo loan.

How do credit scores affect the overall cost of purchasing a Beacon Hill condo?

Credit scores play a crucial role in determining the cost of purchasing a Beacon Hill condo. A higher credit score leads to lower interest rates on mortgages, resulting in significant savings over the life of the loan. For instance, a borrower with a credit score of 760 or above could save around $25,000 in interest payments compared to someone with a score below 620 on a 30-year mortgage for a $300,000 condo. Lenders consider credit scores as an indicator of risk, so it’s essential to maintain good credit to secure the best financing terms and ultimately reduce the overall cost of purchasing a condo in Beacon Hill.

What role do other financial factors, such as income and debt-to-income ratio, play in the approval process for Beacon Hill condo loans?

Other financial factors, such as income and debt-to-income ratio, play a crucial role in the approval process for Beacon Hill condo loans. Lenders assess these factors to determine if borrowers have the means to repay the loan. A higher income indicates a borrower’s ability to make regular payments, reducing the risk for lenders. Similarly, a lower debt-to-income ratio demonstrates that borrowers have manageable levels of debt relative to their income. According to recent data, borrowers with lower debt-to-income ratios are less likely to default on their mortgages, making them more desirable loan candidates for lenders (source: Federal Reserve Bank of Boston).

Do new or existing residents of Beacon Hill condos have different credit score requirements?

Yes, new and existing residents of Beacon Hill condos may have different credit score requirements. New residents who are applying for financing to purchase a condo may face stricter credit score requirements as lenders want to ensure their ability to repay the loan. Existing residents looking to refinance or take out home equity loans may also need to meet certain credit score criteria set by lenders. According to recent data from credit reporting agencies, 76% of approved mortgage loans in Boston require a minimum credit score of 620 or higher, indicating the importance of maintaining a good credit score for both new and existing residents in Beacon Hill condos.

_______________________________________________________________________________________________________________________________

Beacon Hill condos for sale: The importance of your credit score

In the fist two months of 2022, I’ve been working with several Boston Beacon Hill apartment renters and Boston Beacon Hill condo buyers. One thing I can tell you from my experience working with my clients, you are at a major disadvantage for both Beacon Hill apartment renters and Beacon Hill condo buyers if you have a bad credit score.

Boston Beacon Hill condos and the Bottom Line

- If there is anyone left who thinks the Boston condo for sale bubble will burst and prices will come down substantially, let’s note that it would take a multitude of Boston condo for sale buyers with excellent credit scores and what was once a big down payment to give those up.

- The vast majority of today’s Boston Beacon Hill condo buyers have outstanding credit – it would take a disaster for them to walk away.

- Boston condo agents/brokers used to tout how great their buyer’s credit score was – but today it’s expected.

- We don’t need alternative financing any more. Those who don’t qualify are left out of the game

Boston Beacon Hill Condos for Sale in 2024

Beacon Hill condos for sale: The importance of your credit score

Do you want to be able to control and raise your FICO score so you can better qualify for your purchase of a traditional Boston Beacon Hill condo or a modern Boston high rise condo?

Determining your credit score

FICO scoring is like a game and the consumer controls 1/3 of that game. 30% of the credit score is determined by the total amount of revolving credit such as credit cards and department store cards that the consumer has.

For example; if you have a credit card with a $5,000 limit and you owe $4,800 against it, your credit score will go down. If you only owned $1,500 against the $5,000 limit your credit score will increase dramatically.

You will be amazed at how the credit score will change up to or down with just controlling the amount that you charge against your credit card. Remember you are the one who controls that number. This will have a major impact on how much you can afford to buy a Boston Beacon Hill condo for sale

One of the best ways prospective downtown Boston condo buyers can empower themselves when purchasing a home is to improve their buying power. The numbers may seem daunting but identifying ways to strengthen your financial standing will help you each step of the way in your Boston real estate purchase.

When visualizing your dream Boston high rise condo or traditional Beacon Hill home, it’s common for buyers to focus on the physical characteristics. But to mortgage lenders, a home is a numbers game. The following categories related to your buying power demonstrate how lenders identify your financial standing and determine your eligibility for a home purchase.

How to Increase Your Boston Condo Buying Power

As the saying goes, cash is king. The down payment—often 20% of the home’s sale price—can sometimes be the deciding factor between competing offers for a particular downtown Boston condo.

There are numerous benefits to offering a serious down payment. Putting 20% or more down can help your offer stand out, it may allow you to negotiate a lower interest rate on your mortgage and could remove the need for private mortgage insurance (PMI).

Improve Your Real Estate Credit Score

Plain and simple—a better credit score leads to a better interest rate on your mortgage. Your payment history amounts owed, length of credit history, credit mix, and new credit all factor into your credit score. Although improving it will not happen overnight, a higher credit score will pay dividends in the long run.

How to Improve Your Real Estate Credit Score

To improve your credit score, focus on paying down your credit cards, especially those with high interest. Refrain from opening new lines of credit that aren’t necessary and stay away from large purchases leading up to the time when you are preparing to make an offer. Keep in mind that student loans factor into your financial picture. Paying them off consistently will improve your financial standing in the eyes of lenders.

Boston Real Estate Debt-to-Income Ratio

When assessing what you can afford, banks will examine your debt-to-income ratio. Lenders want to know that you’ll be able to pay your mortgage on top of your remaining debt.

They do this by looking at your housing ratio, or front-end ratio, to determine what portion of your income will go to paying your mortgage. Your front-end ratio is calculated by taking your monthly mortgage payment and dividing by your monthly gross income. The higher the ratio, the higher risk of default.

Next, your back-end ratio, or debt-to-income ratio, is used to determine how much of your monthly income goes toward paying your debts. Your back-end ratio is calculated by taking your monthly debt expense (the principal, interest, taxes, and insurance of your mortgage payments, credit card payments, student loans, and any other loan payments), and dividing it by your gross monthly income.

Boston Real Estate and the Bottom Line

Although these aspects of your finances don’t cover everything that goes into the purchase of a home, they do play a significant role in how lenders assess your financial standing and thereby eligibility for approval. Increasing your buying power takes time and strategy. Plan accordingly so that when you find your dream home, you’re in the best position possible to buy it.

Back Bay Boston condos for sale

Beacon Hill Boston condos for sale

Charlestown Boston condos for sale

Navy Yard Charlestown Boston condos

Dorchester Boston condos for sale

Fenway Boston condos for sale

Jamaica Plain Boston condos for sale

Leather District Boston condos for sale

Midtown/Downtown Boston condos for sale

Seaport District Boston condos for sale

South Boston condos for sale

South End Boston condos for sale

Waterfront condos for sale

North End condos for sale

West End condos for sale

East Boston condos for sale

Boston condos for sale near Beacon Hill

Back Bay Boston condos

Beacon Hill Boston condos

Charlestown Boston condos

Navy Yard Charlestown Boston condos

Dorchester Boston condos

Fenway Boston condos

Jamaica Plain Boston condos

Leather District Boston condos

Midtown Boston condos

Seaport District Boston condos

South Boston new condos

South End new condos

Waterfront new condos

North End new condos

West End new condos

East Boston condos

Beacon Hill Office Location

Our office is located in the heart of Beacon Hill at 137 Charles Street. View Beacon Hill condos for sale with photos and recent sales data for the last 30 days.

Click Here: Back to Boston Real Estate Home Search

Back to homepage: Boston condos for sale

Ford Realty – Boston Real Estate Google Reviews 2020 – 2024

Boston Beacon Hill Condos for Sale in 2024

Where is Ford Realty Located?

Ford Realty is located in 137 Charles Street in Beacon Hill