Boston Real Estate for Sale

Boston Downtown/Midtown condos: Using your equity

Boston Midtown condos for sale

Boston Downtown/Midtown condos: Using your equity

Building financial wealth and stability remains one of the top reasons Americans choose to own a home, and as a homeowner, your wealth often grows without you even realizing it. In a recent paper published by the Urban Institute, Home Ownership is Affordable Housing, author Mike Loftin illustrates how homeowners increase their equity and their wealth simply by making monthly mortgage payments:

“The principal portion that reduces the loan balance builds the homeowner’s equity. In doing so, the principal payments behave like an automatic savings account. The principal payment is not money going out; it is money staying in.”

But home equity – the difference between the value of your home and what you currently owe – isn’t just built through your monthly principal payments. Home price appreciation plays a vital role in growing your equity and, ultimately, your wealth.

As Freddie Mac explains:

“Homeownership has cemented its role as part of the American Dream, providing families with a place that is their own and an avenue for building wealth over time. This ‘wealth’ is built, in large part, through the creation of equity…Building equity through your monthly principal payments and appreciation is a critical part of homeownership that can help you create financial stability.”

Homeowners Continue To See Equity Increase

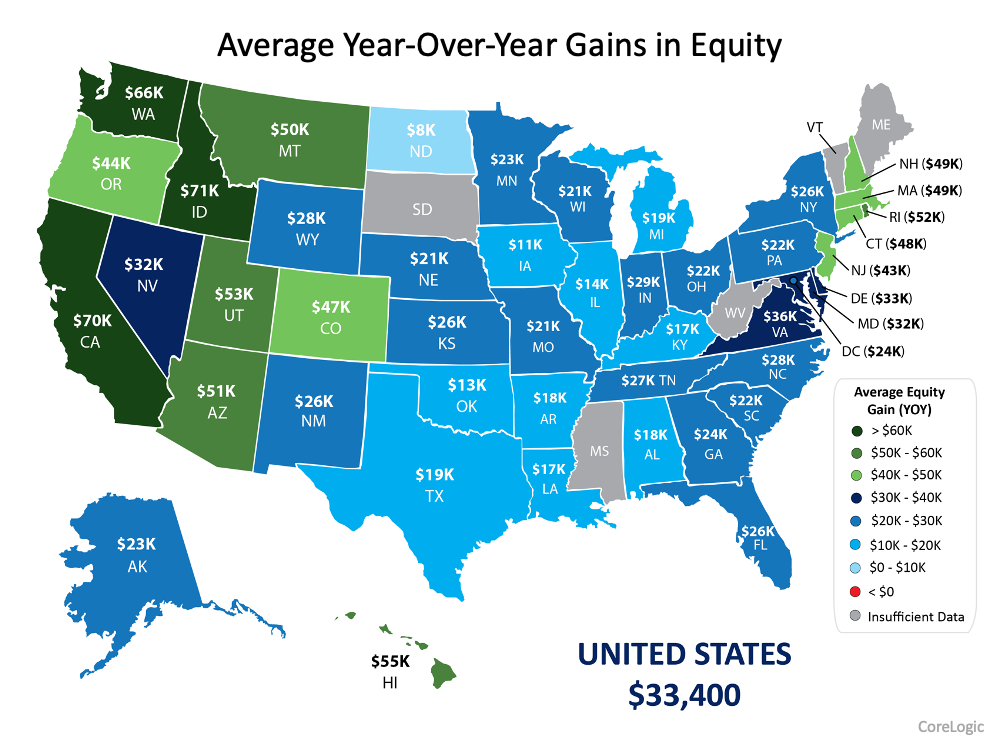

CoreLogic recently published their latest Homeowner Equity Insights Report, and it shows continued growth in equity amidst record home price appreciation. The report provides several key takeaways, all of which point to rising wealth for homeowners:

- The average equity gain of mortgaged homes during the past year was $33,400

- The current average equity of mortgaged homes is greater than $216,000

- There was a 6% increase in total homeowner equity over the past year

- Total U.S. homeowner equity has reached nearly $1.9 trillion

Here, you can see the equity gains by state:

Equity Provides Homeowners with Flexibility

In addition to being a critical tool in building wealth, a homeowner’s equity also provides significant flexibility. When you sell your house, the accumulated equity comes back to you in the sale. Recent increases in home equity coupled with record-low mortgage rates mean it could be the perfect time for homeowners looking to make a move.

Mark Fleming, Chief Economist at First American, notes:

“Existing homeowners today are sitting on record amounts of equity. As homeowners gain equity in their homes, the temptation grows to list their current home for sale and use the equity to purchase a larger or more attractive home.”

Increasing equity also helps families facing challenges brought on by the pandemic. Frank Martell, President and CEO of CoreLogic, explains in the recent Homeowner Equity Insights Report:

“Homeowner equity has more than doubled over the past decade and become a crucial buffer for many weathering the challenges of the pandemic. These gains have become an important financial tool and boosted consumer confidence in the U.S. housing market, especially for older homeowners and baby boomers who’ve experienced years of price appreciation.”

Boston Condo Equity and the Bottom Line

Home equity has always been a powerful wealth-building tool, and homeowners continue to see their financial stability increase. Let’s connect today so you can better understand how much equity you have in your current home or if you’re ready to take the next step in building your savings as a homeowner.

The Least expensive Boston High Rise condos. Asking prices vary every day.

This content is currently unavailable. Please check back later or contact the site's support team for more information.

Boston Real Estate for Sale

Quick — what would you do if you had an extra $100,000?

If your downtown Boston condo owner is in need of major repair, or if you have a life event that could use a cash infusion, you may be looking at taking out a home equity line of credit, refinancing your Boston midtown condominium, or selling. Which is better, and really – what should you be doing with that money?

“Home Equity” is, simply, the cash value that your home has built over time. It’s different than putting money in a piggy bank, because it’s not just the monthly mortgage payments you make — in a strong market like the Downtown Boston condo market your home grows in value just by sitting there. There are a few different ways to access that equity and each has its own advantages and disadvantages. Which one is best for you will depend on what your end goal is.

Home Equity Uses – From Legit to a Bad Idea

A recent CNBC report found that US homeowners gained a collective $570 billion on their homes in 2016. That means 39.5 million homeowners have at least 20 percent equity in their homes, according to Black Knight Financial Services. That’s enough equity to qualify to borrow it back in the form of a refinance or a home equity line of credit.

According to Bankrate.com, the #1 use of home equity is for remodeling. It can be a smart strategy, especially in places like Boston Midtown where the perfect downtown condominium can be hard to come by: Buy a Boston Midtown condo that needs a little work, wait a few years until some of the mortgages has been paid off, then borrow that money back to do the needed remodeling. Keep in mind, sometimes contractors charge their clients based on how busy they are. They are really busy in the summer, but not as much in the fall and winter months.

It makes sense to use home equity to further improve the value of your downtown Boston condo. Homeowners get a little bit more creative in what they spend the money on, though, which can lead to problems down the road, depending on how they are tapping their equity. College education or a career change can be another use of home equity, with the idea of earning more money and paying off the entire home loan sooner. Other borrowers use the cash in their home to reinvest at a higher return than they’re paying in interest. These uses are less advisable, says Bankrate, because of the higher risk. Finally, it is never advisable to use the equity in your home to pay off credit card debt. Doing so does not address the root cause of the financial trouble, and is most likely to result in the loss of your home.

How to Put Your Boston Midtown Home Equity to Work for You

Smart borrowing starts with understanding the different ways you can tap into your home equity. Which can help you out, and which can hurt by putting your Boston Midtown condominium at risk? Finally, would it make more sense to simply sell your home and put some of the equity toward your financial need, and the rest toward another home?

When and How to Refinance Your Home

When you first bought your home, it may not have been under perfect circumstances. Your credit may not have been good enough to qualify you for the best interest rates. You may have taken out an adjustable-rate mortgage that is consistently higher than the fixed-rate options out there. Or, you may been so enthusiastic to own your first home you didn’t think long and hard about the financial implications (and you didn’t have an honest buyers’ agent to keep you from spending more than you could afford!).

Luckily, you can refinance by taking out a new loan for what you currently owe on your home, or for slightly more if you need to tap into some of that home equity.

Refinance loans come in many different stripes and colors. They do have high closing costs, so depending on the loan you could be looking at one to five years to recover the difference between those costs and your current interest rate. Try the refinance break-even calculator, provided by MortgageLoan.com.

If it’s going to take longer to break even than you plan on staying in the Boston downtown home, it would make more sense to wait until you’re ready to sell. Refinancing usually comes with a boatload of fees, while selling your home — especially in this market — can give you immediate financial relief and allow you to start over with a home and a mortgage that works for your budget.

Home Equity Lines of Credit (Usually)

A home equity line of credit is a loan you take out using your Boston Midtown home as collateral. Generally, closing costs are lower on these loans than on a mortgage refinance, but the interest rate is often higher. Because they don’t take quite as long to approve, they are considered a source of “quick cash” for many homeowners. However, they must be paid back quickly to avoid paying more in the long run. In other words, if you are looking to take out a lot of money, be sure you can pay it back quickly with a home equity line or you’ll end up paying a lot in interest over the years.

When Selling Makes Sense

If you are thinking of moving someday anyway, why not start over with a newer Boston Midtown high-rise condo instead of remodeling? You can get the finished product without the hassle. If you are ready to downsize, why not sell and keep some of the extra? Selling your Boston Midtown condominium is a low-risk option. Typically you spend nothing (while the real estate agents spend their own money to market your home) and you only pay if you sell. The balance you’ll earn should be explained upfront and is easy to calculate. There are lot of options to make your transition to a new property as painless as possible.

Contact our sellers’ team today for comparative market analysis. We’ll let you know how much your home can sell for in this market — no fees or charges! This is vital information to have before you make the decision to refinance or take out a line of credit against your home. Right now, homes are selling in 38 days or less in Boston. With reasonable commissions and simple contracts, we make it easy.

View all Midtown condos for sale in this price range

This content is currently unavailable. Please check back later or contact the site's support team for more information.

Click here to view: Boston Midtown condo sales stats

Click here back to Boston Real Estate Home Search

Ford Realty – Boston Real Estate Google Reviews 2021

New Boston Condos for sale just listed TODAY

This content is currently unavailable. Please check back later or contact the site's support team for more information.

Click here back to Boston Real Estate Home Search

Ford Realty – Boston Real Estate Google Reviews 2020/2021