Boston Condos for sale Sale

Is the mortgage broker business model dead?

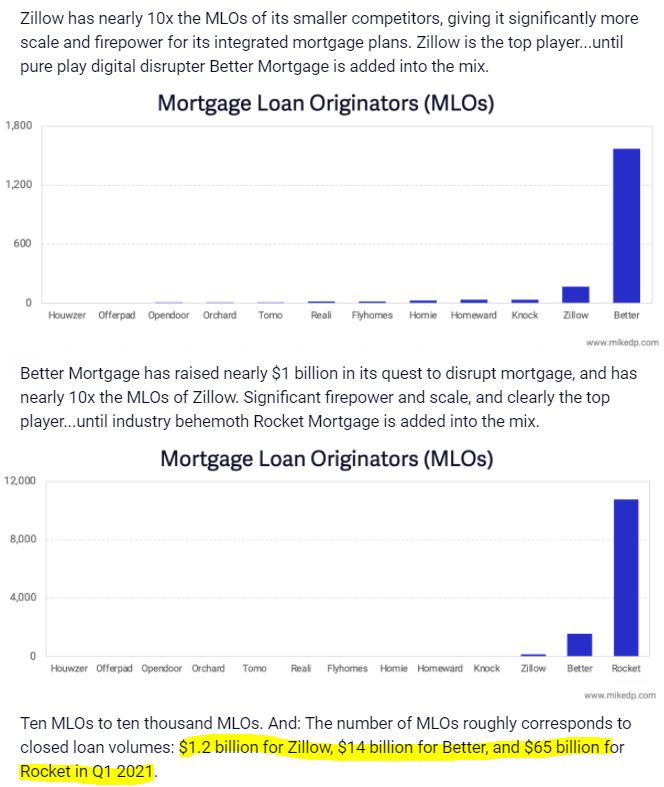

Mike sent out a comparison of mortgage lenders and their quest to disrupt the real-estate-selling business. Here he shows how Rocket is the dominant mortgage lender in the country, and their press release describes their ambition – they think being the jack-of-all-trades will cause them to dominate the space, and now every real estate company will have to offer all services just to keep up. The winners will be determined by who advertises the most:

Boston condo mortgages

Their press release linked here:

Boston Condos for sale Sale

_______________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Earlier this week, one of the largest mortgage brokers in the US shut its doors – not all that uncommon in today’s marketplace. But what was unusual was the candor of the CEO when addressing the challenges of the mortgage broker business model.

“With everything that is going on in the industry, I feel the broker model is dead. With HUD policing 1% origination fee more, the upcoming disclosure of YSP as a fee that is coming out of the borrowers pocket, etc, I think a company really must bank to be competitive.

By enforcing HUD’s requirements and not having the flexibility of a banker to offset it, there are no margins to pay for the proper infrastructure to maintain compliance and QC and have decent margins left. The warehouse line credit is 10% what it used to be so if a company is not a banker already, it is not going to happen.”

For a moment, let’s assume that this CEO is right and that the mortgage broker model is dying – or already dead because it is not profitable.

Is it a good thing if mortgage brokers just go away?

Should the mortgage broker model die will we only be left with the four horseman of the apocalypse, Wells Fargo, Bank of America, JP Morgan Chase, and CitiBank.

Source: The Mortgage Lender via Phoenix real estate blog

Filed Under: Will real estate brokers be next?