Boston Condos for Sale and Apartments for Rent

Did you refinance your Mortgage?

If you didn’t you better move quickly. Boston condo mortgage rates are on the rise

Boston Condos for Sale 2022

Loading...

Did you refinance your Mortgage?

Did you refinance your Mortgage? A large number of downtown Boston condo owners have expressed regret that they missed out on the 2020 refinancing wave, which saw many take advantage of record-low interest rates to reduce their monthly mortgage payments.

Boston real estate refiance

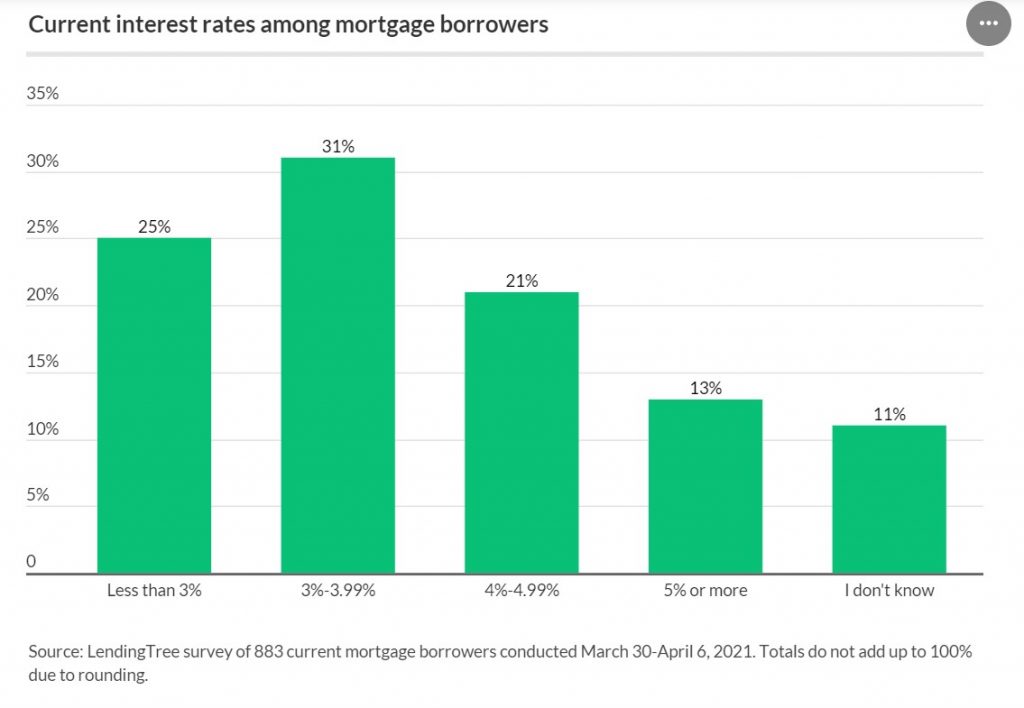

A new survey from LendingTree found that 36% of homeowners who missed the chance to refinance say they regret not doing so.

Many admitted that they missed out due to a lack of knowledge about what refinancing is and what it entails. For instance, some said they falsely believed they had to work with their original lender to refinance, or that it was only possible to refinance once. Some 11% said they don’t even know what their current mortgage rate is and whether or not they could benefit from refinancing.

The most common demographic to take advantage of refinancing

The most common demographic to take advantage of refinancing last year was millennials. Around 42% of people in that bracket did take the opportunity to refinance, compared to just 18% of Generation Xers and 10% of baby boomers.

That said, many homeowners still have an opportunity to take advantage of refinancing. That’s because mortgage rates still remain low, even though they have increased slightly in the last couple of months.

Last week, Freddie Mac said the 30-year fixed-rate mortgage averaged 2.98%, which is still much lower than traditional levels. That could benefit the 34% of homeowners who said they have a mortgage rate of 4% or higher, LendingTree said. Those people could potentially save thousands of dollars over the lifetime of their loan if they refinance now. The message appears to be resonating, with around 49% of homeowners surveyed by LendingTree saying they are considering refinancing within the next 12 months.

Boston real estate refinance

It’s worth noting that there was some good news recently for lower-income homeowners too. Last week, the Federal Housing Finance Agency announced plans for an upcoming program for low-income homeowners with government-backed mortgages to refinance at a lower rate. That plan is set to launch by the summer, and could help low-income borrowers save between $100 to $250 per month on their loan repayments, the FHFA said.

That said, homeowners need to consider the disadvantages of refinancing too. One of the main considerations is that refinancing often results in a new, 30-year term mortgage, which means borrowers could end up paying more over the long term, even if their monthly payments are reduced. Refinancing also comes with closing costs, and usually results in a reduced credit score.

Boston Condos for Sale 2021

Loading...

____________________________________________________________________________________________________________________________________________________________________________

Did you refinance your downtown Boston condo Mortgage?

Home equity appreciation is soaring thanks to the strong Boston real estate seller’s market in the burb. And interest rates remain at a historical low for Boston condo owners. Both are strong reasons motivating homeowners to refinance mortgages and pull out cash. A cash-out refinance replaces your current home loan with a new mortgage that’s higher than your outstanding loan balance (based on a new appraisal). You can use the cash for pretty much anything that you want. Common uses are a major home remodel, consolidating high-interest debt, purchasing a new car, or other financial goals.

Why Refinancing Your Boston Condo Might Make Sense Right Now

After a brief downturn in Boston condos for sale when the coronavirus pandemic began, buyers came back in full force. According to CoreLogic, the average home value increased by 6.6% in the second quarter of this year. That amounts to an average of $9,800 per home. And that is only for the most recent financial quarter. Even amid both the health and economic crisis, median home list prices rose 10.8% compared with last year. Anyone that has not refinanced their mortgage during the last several years is likely to have much more equity built up that can be converted into cash at a very low interest rate.

Boston Condo Mortgage Rates

According to Bankrate, “The average 30-year fixed-refinance rate is 2.97%, down 12 basis points over the last week. A month ago, the average rate on a 30-year fixed refinance was higher, at 3.22%.” If you’re considering shorting the number of years you’ll be paying on your mortgage, the average rate for a 15-year fixed refi is hovering around 2.49%.

New Refinancing Fees

However, not all is rosy for refinancing mortgages. Fannie Mae and Freddie Mac have imposed an “adverse market” fee that begins December 1 (certain refi mortgages are exempt, including those for loan balances below $125,000). This fee is specifically imposed on lenders but is expected to be passed on to borrowers in the form of slightly higher interest rates. The fee is an effort to offset a projected $6 billion in losses related to loans in forbearance with many more loans expected to go into forbearance because the high unemployment rate is expected to continue.

How Cash-Out Refinancing Works

Before filling out that application, be aware that you are not likely to be able to pull 100% of the equity out of your downtown Boston condo. Lenders generally limit the amount you can withdraw to no more than 80% of your home’s value so that you still have an equity cushion.

A mortgage with an outstanding balance of $100,000 but the home appraises at $300,000 will have $200,000 in total equity. At 80% of the equity, you could borrow up to an additional $160,000. The actual amount you receive in cash will be less if you roll application fees, appraisal costs, closing costs, etc. into the new mortgage. Expect to pay about 3% to 5% of the new loan amount for these costs when doing a cash-out refinance. A reasonable expectation is a maximum of $145,000 in cash based on $200,000 of equity.

But this is a new mortgage and you can rewrite the terms and conditions. Maybe your credit score is substantially better than when you took out the original loan. Refinancing to a much lower interest rate will help offset the higher monthly mortgage payment that comes from borrowing more money. If your finances are strong enough, you could refinance to a 15 or 20-year mortgage to shorten the number of years you’ll be paying for your house. Typically, fewer years also means a lower interest rate.

Boston Real Estate and the Bottom Line

But exercise caution. After all, you are putting your home on the line as collateral. If you overextend yourself, there is always the risk of losing your home to foreclosure. Crunch the numbers carefully to be sure a cash-out refinance is the right move for your financial needs. But now might be the right time for a cash-out refinance as a strategic way to improve your overall finances.