Boston condos for sale: Mortgage rate ride of 2024

Boston Condos for Sale and Apartment Rentals

Boston condos for sale: Mortgage rate ride of 2024

If you’re thinking about buying a Boston condo for sale, chances are you’ve got mortgage rates on your mind. You’ve heard about how they impact how much you can afford in your monthly mortgage payment, and you want to make sure you’re factoring that in as you plan your move.

The problem is, with all the headlines in the news about rates lately, it can be a bit overwhelming to sort through. Here’s a quick rundown of what you really need to know.

The Latest on Mortgage Rates

Rates have been volatile – that means they’re bouncing around a bit. And, you may be wondering, why? The answer is complicated because rates are affected by so many factors.

Things like what’s happening in the broader economy and the job market, the current inflation rate, decisions made by the Federal Reserve, and a whole lot more have an impact. Lately, all of those factors have come into play, and it’s caused the volatility we’ve seen. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

Professionals Can Help Make Sense of it All

While you could drill down into each of those things to really understand how they impact mortgage rates, that would be a lot of work. And when you’re already busy planning a move, taking on that much reading and research may feel a little overwhelming. Instead of spending your time on that, lean on the pros.

They coach people through Boston condo market conditions all the time. They’ll focus on giving you a quick summary of any broader trends up or down, what experts say lies ahead, and how all of that impacts you.

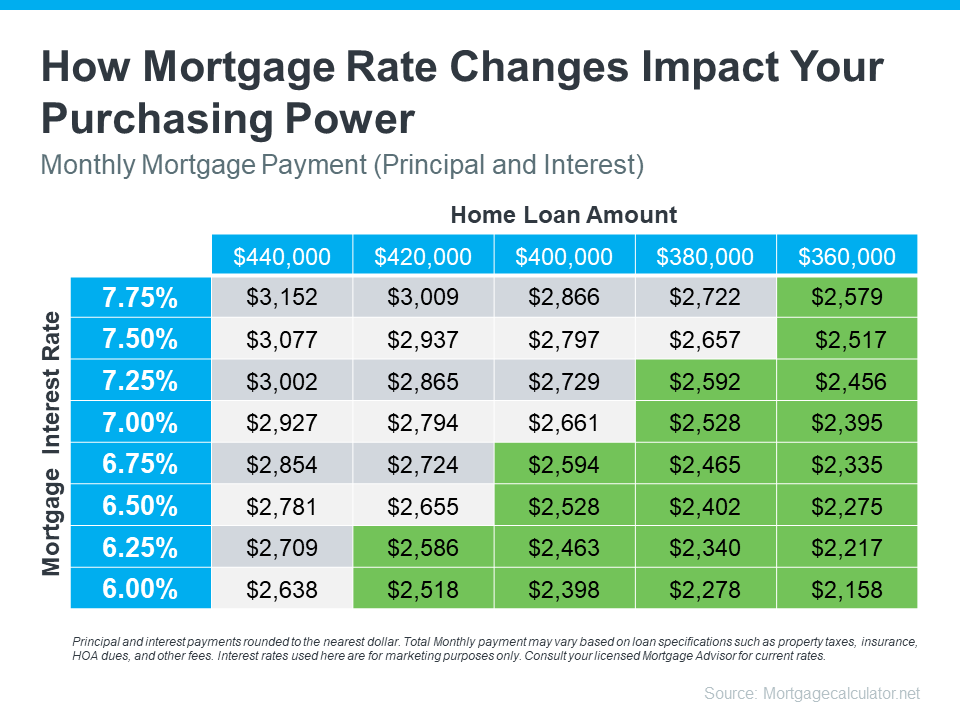

Take this chart as an example. It gives you an idea of how mortgage rates impact your monthly payment when you buy a home. Imagine being able to make a payment between $2,500 and $2,600 work for your budget (principal and interest only). The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

As you can see, even a small shift in rates can impact the loan amount you can afford if you want to stay within that target budget.

It’s tools and visuals like these that take everything that’s happening and show what it actually means for you. And only a pro has the knowledge and expertise needed to guide you through them.

You don’t need to be an expert on real estate or mortgage rates, you just need to have someone who is, by your side.

Boston Condos for Sale Bottom Line

Have questions about what’s going on in the housing market? Let’s connect so we can take what’s happening right now and figure out what it really means for you.

Click Here > Boston Back Bay Apartments for Rent

Back Bay Condos for Sale

This content is currently unavailable. Please check back later or contact the site's support team for more information.

Click Here > Boston Back Bay Apartments for Rent

_____________________

Boston condos for sale: Mortgage rate ride of 2024

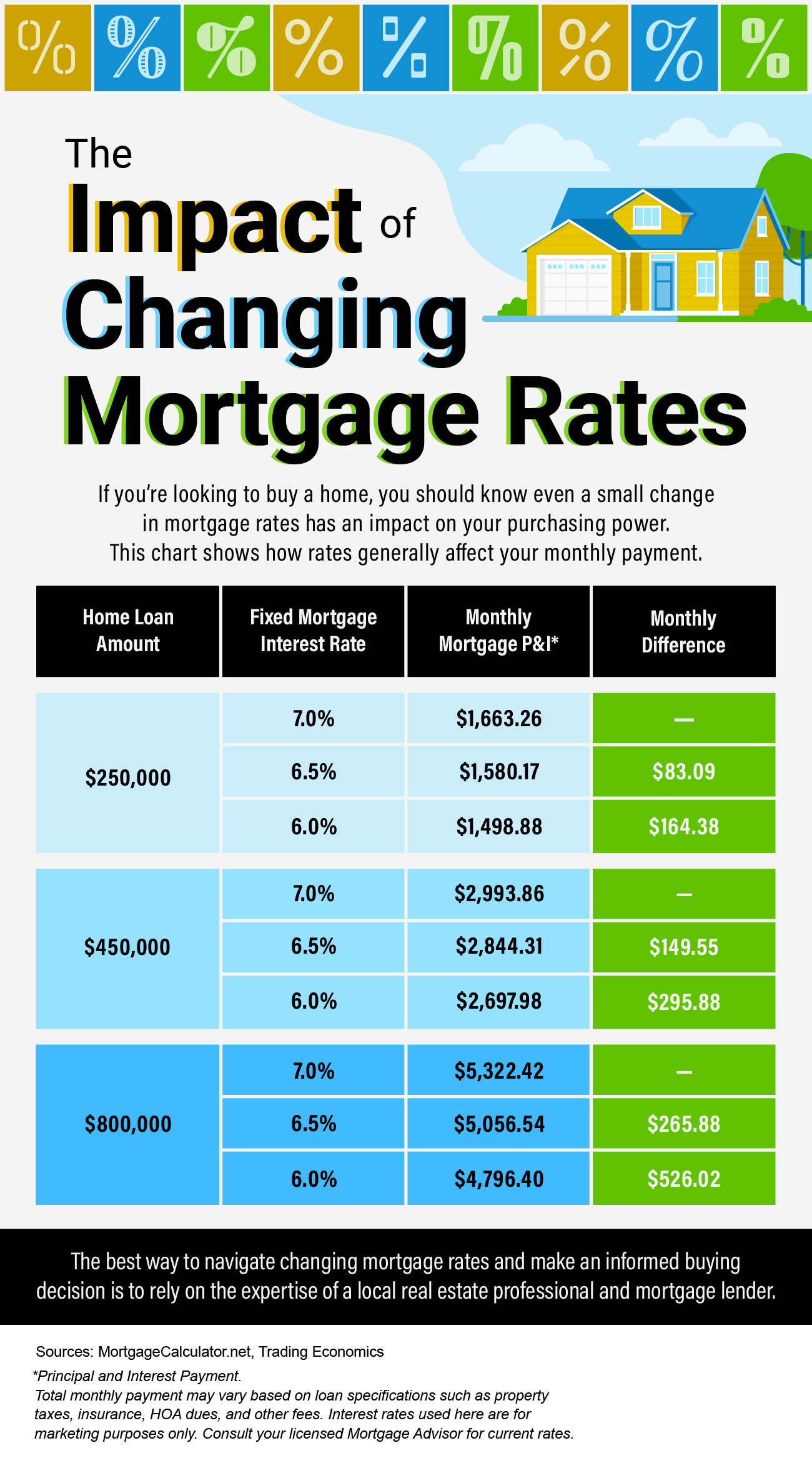

If you’re in the market for a Boston condo for sale in 2023, you’ve must have noticed the mortgage rate ride in the last 12 months. The graph below shows how mortgage rate hikes impact your purchasing power in buying a Boston condo.

Boston Real Estate Blog Updated in 2024

_______________________________________________________________________________________________

Boston condos for sale: Mortgage rate ride of 2024

The mortgage industry had a banner year. Loan originations for 2020 were expected to reach nearly $3.6 trillion, second only to 2003’s all-time high of $3.8 trillion, according to the Mortgage Bankers Association’s December forecast. Refinances fueled the boom as many lenders struggled to keep up with a barrage of homeowners taking advantage of record low rates.

Let’s face it: we’re not made of money! That’s why the ability to borrow cash in the Boston downtown real estate market is a crucial aspect of buying and selling Boston condos for sale

Most people borrow that cash with a mortgage, and every mortgage comes with an interest rate. Mortgage rates have been in the news recently: First they were falling to historic lows, then we started seeing headlines about a “surge”. When that happens, those of us in the real estate business start looking at how the changing mortgage rate will affect Boston condo for sale prices, buyer activity, and seller confidence. Most important, will mortgage rates go up or down in 2018 and at the start of 2019, and how will this affect the Boston midtown condo market.

Boston Condo Mortgage Mechanics

Mortgage rates and the real estate market are connected in a number of ways, and with all of the acronyms, percentages and types of mortgages out there, it can get very confusing very quickly. That’s probably why most Beacon Hill condo buyers I meet in my Beacon Hill real estate office don’t understand all of the dynamics. But they should try — in real estate, timing is everything. In this post, we’ll delve into what the experts are predicting will happen to mortgage rates and buying power in the new year. Then we’ll apply it to the local market so that you can better understand how mortgage rates influence Boston condos for sale whether you’re buying or selling a home this year.

The Boston Real Estate Rate Roller Coaster

Simple fact about mortgage rates: They go up and down. And, when mortgage rates go up, typically, the real estate market slows down a bit. That’s because mortgage rates directly impact what a buyer can afford to pay for a Boston condo for sale. A higher mortgage rates means buyers are paying more interest. If your lender is charging you more interest, it takes a bigger chunk of your available income, meaning you’ll have less to put toward the home itself. That’s why real estate agents monitor mortgage rates — and develop close relationships with local lenders to help insure their clients are getting the best deal possible.

The Average Mortgage Rate: Down, down, down, up?

Technically, any lender can set any interest rate they like, and rates will always vary based on the length of the loan, the amount, the borrower’s credit score, etc. So how do we get a picture overall of what mortgage rates are doing?

Most analysts look at the Federal Housing Administration’s mortgage rate as a baseline. Specifically, they monitor the average rate for Freddie Mac’s 30-year mortgage, a common type of mortgage. When I say “average mortgage rate” in this article, that’s the one I’m referring to.

Lately, there have brought a fair amount of excitement to the mortgage rate world. The average mortgage rate had generally been fluctuating up and down.

If you looked at the news about mortgage rates in the last couple of days they have risen

What caused this rise? Many factors influence the mortgage rates, but most analysts said that it was either an investor reaction to the election, or the mortgage industry was raising rates in anticipation of a Federal Reserve rate hike, or some combination of both.

Mortgages Rates and Boston Condos for Sale

It’s hard to point to a specific point where rates are “too high”. In fact, it’s the job of the Federal Reserve to try to balance mortgage rates and buyer activity. When we’re seeing a hot housing market like we have in downtown Boston right now, the natural reaction would be to increase rates and slow down that activity. If activity dies down, like it did during the housing market crash of ‘09, it makes sense to lower rates (which is exactly what the Federal Reserve did). Now, no one expects that type of crash again, anytime soon.

It’s not a perfect system, and there may be a delay of months or even years before mortgage rates move in the direction they “should”. With an increase in mortgage rates, not only do buyers think to themselves “I should wait to buy a home until they go down a bit,” but sellers also tend to wait to put their home on the market.

A Great Time to Buy or Sell a Boston Condo

Right now, it would be hard for mortgage rates to be much lower, and as we saw in the last couple of months, any kind of shift in the political or economic climate is liable to send them climbing again. It might not be this year or next, but what we do know is that with interest rates at 3% or below, many buyers are not seeing the barriers to entry that they had five years ago, and they’re jumping on the Boston Beacon Hill condo market! So what are you waiting for? Call the number one real estate team in downtown Boston condo team and let’s talk.