Boston Condo for Sale Search

Missing Mortgage Payments: Forbearance Can Help

Missing Mortgage Payments: Forbearance Can Help. Over the past year, the pandemic made it challenging for some homeowners to make their mortgage payments. Thankfully, the government initiated a forbearance program to provide much-needed support. Unless they’re extended once again, some of these plans and the corresponding mortgage payment deferral options will expire soon. That said, there’s still time to request assistance. If your loan is backed by HUD/FHA, USDA, or VA, you can apply for initial forbearance by June 30, 2021.

Recently, the Consumer Finance Institute of the Federal Reserve Bank of Philadelphia surveyed a national sample of 1,172 homeowners with mortgages. They discussed their familiarity with and understanding of lender accommodations that might be available under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The results indicate that some borrowers didn’t take advantage of the support available through forbearance:

“Most borrowers who had not used forbearance during the pandemic reported that it was because they simply did not need it. However, among the remainder, a lack of understanding about available accommodations may also be playing a role. Around 2 out of 3 in this group reported not seeking forbearance because they were unsure or pessimistic about whether they would qualify — even though a high fraction of borrowers are eligible for forbearance under the Coronavirus Aid, Relief, and Economic Security (CARES) Act.”

Here are some of the reasons why those borrowers didn’t opt for forbearance:

- They were concerned forbearance may be costly

- They didn’t understand how to request forbearance

- They didn’t understand how the plans worked and/or whether they would qualify

If you have similar questions or concerns, the following answers may ease your fears.

If your concerned forbearance may be costly:

The Consumer Financial Protection Bureau (CFPB) explains:

“For most loans, there will be no additional fees, penalties, or additional interest (beyond scheduled amounts) added to your account, and you do not need to submit additional documentation to qualify. You can simply tell your servicer that you have a pandemic-related financial hardship.”

It’s important to contact your mortgage provider (the company you send your mortgage payment to every month) to explain your current situation and determine the best plan available for your needs.

If you’re not sure how to request forbearance:

Here are 5 steps to follow when requesting mortgage forbearance:

- Find the contact information for your servicer

- Call your servicer

- Ask if you’re eligible for protection under the CARES Act

- Ask what happens when your forbearance period ends

- Ask your servicer to provide the agreement in writing

If you don’t understand how the plans work and/or whether you will qualify:

This is how the Consumer Financial Protection Bureau (CFPB) explains the program:

“Forbearance is when your mortgage servicer or lender allows you to pause or reduce your mortgage payments for a limited time while you build back your finances…

Forbearance doesn’t mean your payments are forgiven or erased. You are still obligated to repay any missed payments, which, in most cases, may be repaid over time or when you refinance or sell your home. Before the end of the forbearance, your servicer will contact you about how to repay the missed payments.”

The CFPB also addresses who qualifies for forbearance relief:

“You may have a right to a COVID hardship forbearance if:

- You experience financial hardship directly or indirectly due to the coronavirus pandemic.

- You have a federally backed mortgage, which includes HUD/FHA, VA, USDA, Fannie Mae, and Freddie Mac loans.

For mortgages that are not federally backed, servicers may offer similar forbearance options. If you are struggling to make your mortgage payments, servicers are generally required to discuss payment relief options with you, whether or not your loan is federally backed.”

Boston Real Estate and the Bottom Line

Like many Americans, your home may be your biggest asset. By acting quickly, you might be able to take advantage of critical relief options to help keep you in your home. Even if you tried to apply at the beginning of the pandemic and it for some reason didn’t work out, try again. Contact your mortgage provider today to determine if you qualify. If you have additional concerns, let’s connect to answer your questions and determine if there are other mortgage relief options in our area as well.

Boston Condo for Sale Search

____________________________________________________________________________________________________________________________________________________________________________

Missing Mortgage Payments: Forbearance

Mortgage forbearances for homeowners affected financially by the pandemic declined slightly over the past week. Black Knight said that there were 200,000 plans scheduled to expire at the end of November, probably accounting for the majority of the 39,000-loan downturn in the various forbearance programs. Another 1 million plans are due to expire at the end of this month.

As of December 1, there were a total of 2.76 million loans remaining in plans, 5.2 percent of the 53 million active mortgages in servicer portfolios and representing $561 billion in unpaid principal. Eighty-one percent of those loans have had their terms extended at some point since March.

The number of GSE (Fannie Mae and Freddie Mac) loans in forbearance dropped by 25,000 during the week, leaving a total of 967,000 homeowners remaining in plans. This is 3.5 percent of the companies’ combined portfolios. FHA and VA loans decreased by 14,000 units to a total of 1.118 million or 9.2 percent of those loans. Loans serviced for bank portfolios or private label securities held steady at 677,000 loans or 5.2 percent of the total. There are 91,000 fewer loans in forbearance plans than one month ago, a 3.2 percent decline.

Updated: Boston real estate for sale forbearances 2020

Originally, some housing industry analysts were concerned that the mortgage forbearance program (which allows families to delay payments to a later date) could lead to an increase in foreclosures when forbearances end. Some even worried that we might relive the 2006-2008 housing crash all over again. Once you examine the data, however, that seems unlikely.

As reported by Odeta Kushi, Deputy Chief Economist for First American:

“Despite the federal foreclosure moratorium, there were fears that up to 30% of homeowners would require forbearance, ultimately leading to a foreclosure tsunami. Forbearance did not hit 30%, but rather peaked at 8.6% and has been steadily falling since.”

According to the most current data from Black Knight, the percentage of homes in forbearance has fallen to 7.4%. The report also gives the decrease in raw numbers:

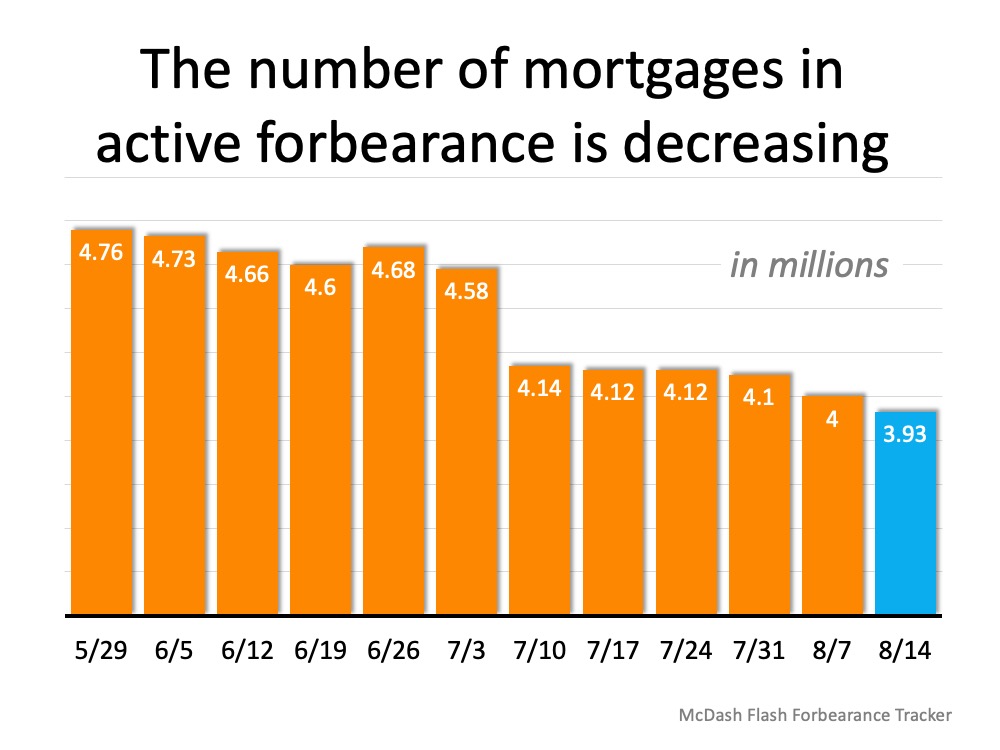

“The overall trend of incremental improvement in the number of mortgages in active forbearance continues. According to the latest data from Black Knight’s McDash Flash Forbearance Tracker, the number of mortgages in active forbearance fell by another 71,000 over the past week, pushing the total under 4 million for the first time since early May.”

Here’s a graph showing the decline in forbearances over the last several months: The report also explains that across the board, overall forbearance activity fell with 10% fewer new forbearance requests and nearly 40% fewer renewals.

The report also explains that across the board, overall forbearance activity fell with 10% fewer new forbearance requests and nearly 40% fewer renewals.

What about potential foreclosures once forbearances end?

Kushi also addresses this question:

“There are two main reasons why this crisis is unlikely to produce a wave of foreclosures similar to the 2008 recession. First, the housing market is in a much stronger position compared with a decade ago. Accompanied by more rigorous lending standards, the household debt-to-income ratio is at a four-decade low and household equity near a three-decade high. Indeed, thus far, MBA data indicates that the majority of homeowners who took advantage of forbearance programs are either staying current on their mortgage or paying off the loan through a home sale or a refinance. Second, this service sector-driven recession is disproportionately impacting renters.”

There is one potential challenge in the Real Estate Market

Today, the options available to homeowners will prevent a large spike in foreclosures. That’s good not just for those families impacted, but for the overall housing market. A recent study by Fannie Mae, however, reveals that many Americans are not aware of the options they have.

It’s imperative for potentially impacted families to better understand the mortgage relief programs available to them, for their personal housing situation and for the overall real estate market.

Boston Real Estate and the Bottom Line

If Americans fully understand their options and make good choices regarding those options, the current economic slowdown does not need to lead to mass foreclosures.

Boston Condo for Sale Search