Boston condos for sale: What credit score do you need to buy a condo?

Boston Condos for Sale and Apartments for Rent

Boston condos for sale: What credit score do you need to buy a condo?

Boston condos for sale: What credit score do you need to buy a condo? According to Fannie Mae, 90% of buyers don’t actually know what credit score lenders are looking for, or they overestimate the minimum needed.

Let that sink in. That means most Boston condo for sale buyers think they need better credit than they actually do – and maybe you’re one of them. And that could make you think buying a home is out of reach for you right now, even if that’s not necessarily true. So, let’s look at what the data really says about credit scores and homebuying.

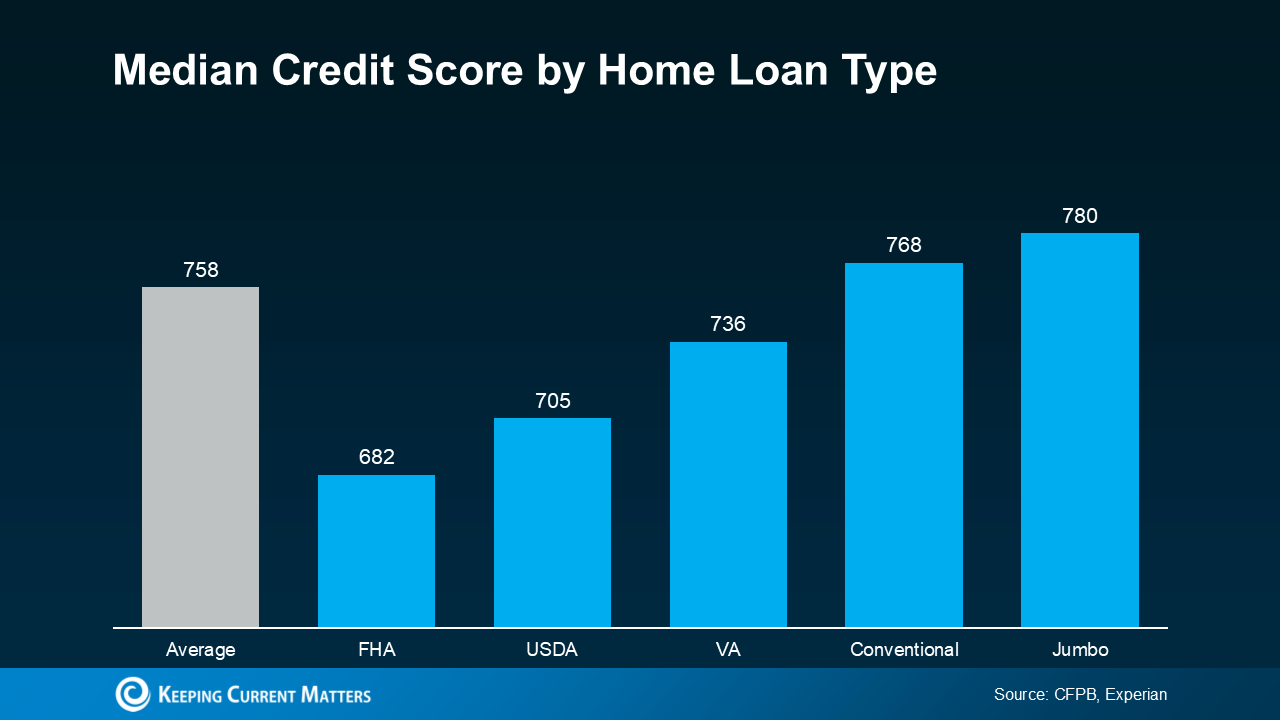

What credit score do you need to buy a condo? There’s No One Magic Number

There’s no universal credit score you absolutely have to have when buying a home. And that means there’s more flexibility than most people realize. Check out this graph showing the median credit scores recent buyers had among different home loan types:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

Why Your Score Still Matters

When you buy a home, lenders use your credit score to get a sense of how reliable you are with money. They want to see if you typically make payments on time, pay back debts, and more.

Your score can impact which loan types you may qualify for, the terms on those loans, and even your mortgage rate. And since mortgage rates are a big factor in how much house you’ll be able to afford, that may make your score feel even more important today. As Bankrate says:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That still doesn’t mean your credit has to be perfect. Even if your credit score isn’t as high as you’d like, you may still be able to get a home loan.

Want To Boost Your Score? Start Here

And if you talk to a lender and decide you want to improve your score (and hopefully your loan type and terms too), here are a few smart moves according to the Federal Reserve Board:

- Pay Your Bills on Time: This is a big one. Lenders want to see you can reliably pay your bills on time. This includes everything from credit cards to utilities and cell phone bills. Consistent, on-time payments show you’re a responsible borrower.

- Pay Down Your Debt: When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible. That makes you a lower-risk borrower in the eyes of lenders – making them more likely to approve a loan with better terms.

- Review Your Credit Report: Get copies of your credit report and work to correct any errors you find. This can help improve your score.

- Don’t Open New Accounts: While it might be tempting to open more credit cards to build your score, it’s best to hold off. Too many new credit applications can lead to hard inquiries on your report, which can temporarily lower your score.

Boston Condos for Sale and the Bottom Line

Your credit score doesn’t have to be perfect to qualify for a Boston condo for sale loan. But a better score you get better terms on your home loan. The best way to know where you stand and your options for a mortgage is to connect with a trusted lender.

Boston condos for sale: What credit score do you need to buy a condo?

According to data from the most recent Origination Insight Report by Ellie Mae, the average FICO® score on closed loans reached 753 in February. As lending standards have tightened recently, many are concerned over whether or not their credit score is strong enough to qualify for a mortgage. While stricter lending standards could be a challenge for some, many buyers may be surprised by the options that are still available for borrowers with lower credit scores.

Boston real estate and credit score

The fact that the average Boston condo buyer has seen their credit score go up in recent years is a great sign of financial health. As someone’s score rises, they’re building toward a stronger financial future. As more Boston downtown condo buyers with strong credit enter the housing market, we see a natural increase in the FICO® score distribution of closed loans, as shown in the graph below:If your credit score is below 750, it’s easy to see this data and fear that you may not be able to qualify for a mortgage. However, that’s not always the case. While the majority of borrowers right now do have a score above 750, there’s more to qualifying for a mortgage than just the credit score, and there are still options that allow people with lower credit scores to buy their dream home. Here’s what Experian, a global leader in consumer and business credit reporting, says:

- Federal Housing Administration (FHA) loans: “With a 3.5% down payment, homebuyers may be able to get an FHA loan with a 580 credit score or higher. If you can manage a 10% down payment, though, that minimum goes as low as 500.”

- Conventional loans: “The most popular loan type typically comes with a 620 minimum credit score.”

- S. Department of Agriculture (USDA) loans: “In general, lenders require a minimum credit score of 640 for a USDA loan, though some may go as low as 580.”

- S. Department of Veterans Affairs (VA) loans: “VA loans don’t technically have a minimum credit score, but lenders will typically require between 580 and 620.”

There’s no doubt a higher credit score will give you more options and better terms when applying for a mortgage, especially when lending is tight like it is right now. When planning to buy a home, speaking to an expert about steps you can take to improve your credit score is essential so you’re in the best position possible. However, don’t rule yourself out if your score is less than perfect – today’s market is still full of opportunity.

Boston condos for sale: What credit score do you need to buy a condo?

When you first start looking into financing a Boston condo for sale, you’ll quickly learn your credit score makes a huge difference. This three-digit number is essentially a calculation of how likely you are to repay a loan. Even if you’ve never checked your score before, it still exists and can either help or harm you when purchasing property. Whether you’re looking at Boston Beacon Hill homes or Boston downtown high-rise condo, read on to discover how your credit score could affect your ability to buy a home.

Boston Condo Buyer 550 & Lower

This is considered a bad credit score. You may not even qualify for standard FHA loans, which are often the recommended loan type for people with poor credit. Those who can get an FHA loan need to have a score of at least 500, and they’ll have to pay a down payment of 10 percent. A higher down payment is required because it’s a bigger risk for lenders.

Boston Condo Buyer 550 to 649

Once you get into this category, your credit score still isn’t ideal, but you’re not in such a bad position. You can qualify for an FHA loan with only a 3.5 percent down payment once your score hits 580, and if your score is at least 620, you can even get normal housing loans backed by Fannie Mae and Freddie Mac. In general, anyone with a credit score of at least 600 will be able to find some reasonable mortgage options.

Boston Condo Buyer 650 to 699

Most Boston Midtown condo buyers tend to fall in the upper 600s. You might find your interest rates are a little higher, costing about .5 percent on average more than the company’s lowest interest rate offerings. However, most lenders will still be willing to work with you, and it shouldn’t be particularly challenging to get a home. You may find you can get more favorable rates by being willing to pay a higher down payment.

Boston Condo Buyer 700 to 749

All loaning institutions see people with credit scores of 700 or higher as having good scores, which puts them in a far better position when shopping for loans. Since lenders see you as being decently reliable and likely to pay off your loan on time, you’ll have access to lower down payment options and lower interest rates.

Boston Condo Buyer 750 & Higher

If your credit score is in this range, you’re one of the rare people with excellent credit. Lenders love working with those who have excellent credit because they feel like it’s a wise investment. You can expect to get interest rates as much as two percent lower than people with poor credit. Those with excellent credit are also far less likely to have to pay hefty fees or high mortgage insurance rates when settling on a loan.

Boston Real Estate and the Bottom Line

Don’t let assumptions about whether your credit score is strong enough put a premature end to your homeownership goals. Let’s connect today to discuss the options that are best for you.

If you’re interested in purchasing downtown Boston real estate is an area that always has a variety of Boston condos for sale available, and if you aren’t happy with the initial interest rate on your home loan, you can take advantage of the opportunity to refinance later. The experienced agents at Ford Realty can help you start your search for the perfect property. Call us at 617-595-3712.

Boston Real Estate

View Boston Seaport condos for sale

Boston condos for sale

Charles River Park condos for sale

Ford Realty Beacon Hill – Condo for Sale Office

Boston condos for sale – Ford Realty Inc

Updated: Boston Condos for Sale Blog 2025

Byline – John Ford Boston Beacon Hill Condo Broker 137 Charles St. Boston, MA 02114

Boston Condos for Sale

Loading...

Ford Realty Inc., Charles Street, Beacon Hill