Boston real estate for sale search

How to solve the housing crisis, in Boston, and nationwide

I had originally planned on writing a very long, in-depth entry about the housing market, cost of housing, affordable housing, etc. Instead, I think I’ll go have a full body wax.

Therefore, in brief, here’s how I feel about the state of the housing market, in our city, and nationwide.

There is a problem with affordability in our city, because of the simple economic theory of supply and demand. Demand increased, over the past couple of years, for a variety of reasons, plus, for some reason that could not be explained away by economists; this may have been buyer euphoria (psychosis), the wealth effect, whatever.

Now, even though the market has cooled (in sales volume), I don’t expect there will be much of a drop in average and median sales prices, at least here in Boston. Nationwide, we may see more significant drops, in areas such as Florida, parts of California, Las Vegas, etc., but still, prices may only fall 10% or so.

That’s not going to help the first-time homebuyer.

This problem with the first-time homebuyer will have a domino effect, as owners higher up on the housing scale won’t be able to sell in order to buy something bigger, better, and more expensive.

(A good question to ask is, what percentage of Americans want to own, ever – we’re just under 70% ownership in this country. This is the highest rate, ever, in recorded US history. Is it also the upper limit? The rest of the people out there could be students, and old, sick people – they aren’t going to buy, ever.)

One thing I know for sure is that the solution to this “housing crisis” is not set-asides, much as politicians would prefer. (Boston has an “affordable” housing set-aside of 13%, (I think), which has done nothing to lower the price of housing in the city, and, in my opinion, doesn’t help anyone, buyers included.) Must I add, the solution is not rent control or rent stabilization, or whatever fun name your city councilor calls it.

It’s an increasing supply.

The city of New York is actively involved in increasing the number of “affordable housing” units, read, affordable to “middle class” people. I don’t agree with their methods, but I do admire Mayor Bloomberg’s effort. He wants NYC to build 165,000 more units of housing affordable to lower and middle class people, over the next decade. This is privately owned housing, not projects.

Unlike Boston, NYC funds new housing by giving developers tax breaks, called the 421-a program. The new buildings are taxed at their old tax rate, for 25-years, in some cases. The properties are not re-assessed. That’s a bundle of money in the pockets of new owners.

Much of Manhattan is covered by this program, and there is no upper limit on the benefit – you can buy a $2 million condo, and you don’t pay more (percentage-wise) than someone buying a $250,000 condo.

This was obviously a windfall to new owners, and the city is now attempting to put limits on who can use the benefit, where, and how much. The city might also only allow the tax benefit to be used by developers who include low-priced units in their buildings (or, construct buildings full of low-priced units, I’m not sure which). (My understanding is that there are already “exclusion zones” in NYC, where developers have to build lower-priced units. These zones may be expanded, under the revised proposal.)

In Boston, the city has a more “stick” than the “carrot” approach. Every developer has to set aside a certain number of units in each building for “affordable housing” units. It’s “affordable housing” in quotes, because, one, the units built are luxury, in many ways, plus, buyers can qualify for these units, even though they may have household incomes in the $70,000 – $90,000 range.

It’s inefficient and ineffectual. And, it doesn’t help anyone. Buyers of these units find they have a hard time selling, at least they have in the past, because the pool of potential buyers is limited, implicitly. Plus, can anyone really say that the housing crisis has been solved, in any way, because of this program? No.

One possible way for states and cities to help homebuyers, without messing with the private market, is to give cold hard cash to people, within certain income ranges.

New York state is experimenting with this.

In Long Island, there are few houses affordable, even to those making 30 percent more than the median area income, according to an article in the New York Times.

One popular program is for first-time homebuyers.

This money will be available to people who earn up to 130 percent of the median income; previously, the income limit was 120 percent of the median. The program now helps with homes priced up to $450,000; that is $60,000 more than the previous maximum.

A buyer can tap into this fund only if his or her employer makes an initial contribution toward the home purchase — $3,000 to $10,000, depending on the company’s size.

The company then applies for grant money up to three times their contribution. The money can be used for a down payment. In addition, up to $20,000 is available to fund renovations on the buyers’ new homes.

Effective Jan. 1, the new grant money will be available to a single person earning as much as $82,800 annually, a couple earning $94,650 and a family of four earning $118,300.

You can see how this helps. It truly puts homeownership in the hands of those who would otherwise be unable to afford to buy, because they lack the downpayment, even if they can afford the monthly payments.

In addition, these homebuyers get a lower interest rate, and, and one of the state’s mortgage programs will pay closing fees, a year of homeowner’s insurance, and six months of taxes.

Program participants in their new houses at least 10 years or pay back the fees. (DAMN!)

In theory, I like the idea. However, on a certain level, it seems unfair to me that certain people get a benefit, while others don’t, regardless of income. I also have a problem with the government getting involved in what is purely a private market matter.

Again, in my opinion, supply and demand are all that we need to focus on. It’s imperfect, but it’s reality. In my world. Still, I think it deserves more thought.

I guess what I’m saying is, these problems don’t solve the housing crisis, they deal with its effects.

(The ways to solve the housing crisis include increasing supply or restricting demand. Rising prices restrict demand, cities’ and states’ building regulatory hurdles restrict demand, higher mortgage rates restrict demand, recessions restrict demand.)

Well, another thing to keep in mind is that the downtown Boston, Boston Proper, area, is the most desirable in the city. Exactly how much housing can be built here, anyway, without us facing huge high-rises at every street corner? (I wish.)

I think we need to look at the waterfront for clues as to what might happen, in our future. Over the coming three to seven years, this area, the Seaport District, will see enormous growth, in residential, commercial, and office space. Incredible. Jaw-dropping. And, unprecedented since the Back Bay was fiilled in, between 1839 and 1871 (w/e).

First, and foremost, it is a mistake to force developers to include affordable housing in their new projects. Ridiculous. These buildings are adding residents, homeowners, where there were none, before. These new owners are paying property taxes, increasing the city’s revenues, where before there were none. Let the free market reign.

Other articles of interest to you may be these two stories – the first article, from the Times, is about the sale of the Stuyvesant Town and Peter Cooper Village, two adjoining complexes on First Avenue between 14th and 23rd Streets.

Built by Metropolitan Life in 1947 for returning veterans, Stuyvesant Town and Peter Cooper Village have served as an affordable redoubt for generations of police officers, teachers, nurses, and the like.

The 110 buildings have just been sold, and, presumably, the new owners will be looking for ways to increase the return on their investment, perhaps by bringing some of the below-market rentals up to market-rate, and perhaps by converting some buildings into condos (more likely, teardowns?).

Also, this article, a blog entry, discusses the conversion of Montreal’s former Imperial Tobacco factory and headquarters into condos.

The complex, which has stood in the working-class neighborhood of St. Henri for more than a century, has been empty since 2003 when Imperial shut down the last of its operations, putting several hundred neighborhood residents out of work.

[The] Imperial project is different. Since its entry prices are so low, it won’t attract your typical yuppie crowd. If anything, the combination of cheap units and social housing will ensure a nice balance of residents. It will take some of the pressure off of the neighbourhood’s existing housing stock, too, helping to curb condo conversions. The emphasis on bicycle parking and car-sharing, combined with the project’s proximity to Lionel-Groulx metro, a major transfer station, means it will encourage pedestrian activity in what until now has been a particularly forlorn part of St. Henri.

St. Henri’s location, architecture, and historical ambiance make it a very desirable neighborhood, however. That’s why, if the demand for new condos is to be accommodated, it should take the form of the Imperial Tobacco project: affordable, respectful of its neighborhood, and ecologically sound.

The Imperial project does include set-asides, which I don’t agree with, but it sounds like it was the only way to get it approved. Who benefits from the new housing? Um, everyone?

Here is a neat little story about three post-college kids who decided to buy a piece of distressed land, in downtown Oberlin, and build on it. Shows how simple it is to make things work if you’re determined.

Ben Ezinga, Joshua Rosen, and Naomi Sabel spent their first four years as typical liberal arts college students, going to class, writing papers and looking forward to graduation. Their last four years in Oberlin, however, have been spent learning hard lessons in real estate.

Against long odds, the once young, naïve and inexperienced team is nearing the groundbreaking on the first major commercial development in the historic downtown since 1958. They hope they are building not just a mixed-use project, but a model for progressive urban redevelopment under financially difficult circumstances.

[There will be] a combination of 49 residential units, 14 of which will be rented at affordable prices and the rest offered for sale; 12,000 square feet of street-level retail space, which will be leased only to local proprietors; 10,000 square feet of publicly accessible open space where concerts and markets will be held; and both underground and surface parking.

So, as you can see from above, a real problem exists, and there are several ways that cities are attempting to deal with it.

Boston real estate for sale search

_______________________________________________________________________________________________________________________________________________________________________________________________________

There are many non-financial benefits of buying your own home. However, today’s headlines seem to be focusing primarily on the financial aspects of homeownership – specifically affordability. Many articles are making the claim that it’s not affordable to buy a home in today’s market, but that isn’t the case.

Today’s buyers are spending approximately 20% of their income on their monthly mortgage payments. According to The Essential Guide to Creating a Homebuying Budget from Freddie Mac, the 20% of income that purchasers are currently paying is well within the 28% guideline suggested:

“Most lenders agree that you should spend no more than 28% of your gross monthly income on a mortgage payment (including principal, interest, taxes and insurance).”

So why is there so much talk about challenges regarding affordability?

It’s Not That Homes Are Unaffordable – It’s That They’re Less Affordable.

Since home prices are rising, it’s true that homes are less affordable than they have been since the housing crash fifteen years ago. Headlines making these claims aren’t incorrect; they just don’t tell the whole story. To paint the full picture, you have to look at how today stacks up with historical data. A closer analysis of affordability going further back in time reveals that homes today are more affordable than any time from 1975 to 2005.

Despite that, the chatter about affordability is pushing some buyers to the sidelines. They don’t feel comfortable knowing someone else got a better deal a year ago.

However, Are Homes Really Less Affordable if We Consider Equity?

In a recent post, Odeta Kushi, Deputy Chief Economist at First American, offers a different take on the financial components of housing affordability. Kushi proposes we should at least consider the impact equity build-up has on the affordability equation, stating:

“For those trying to buy a home, rapid house price appreciation can be intimidating and makes the purchase more expensive. However, once the home is purchased, appreciation helps build equity in the home, and becomes a benefit rather than a cost. When accounting for the appreciation benefit in our rent versus own analysis, it was cheaper to own in every one of the top 50 markets.”

Let’s look at an example. In the above-mentioned post, Kushi examines the rent versus buy situation in Dallas, Texas. Kushi chose Dallas because home prices there sit near the median of the top 50 markets in the nation.

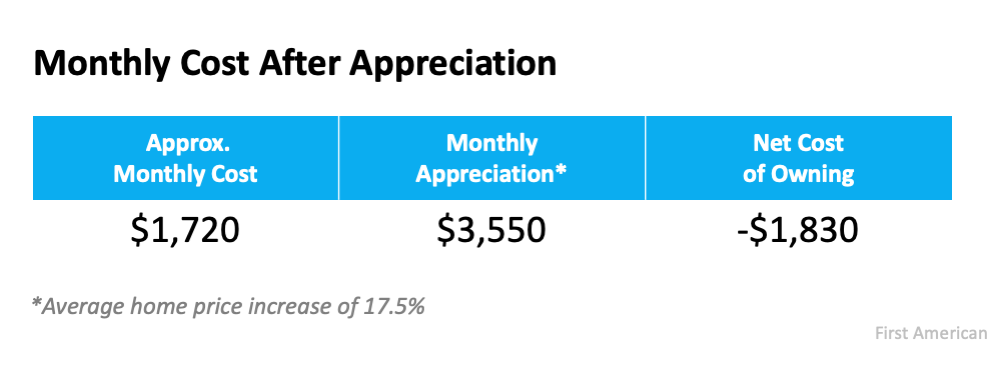

Kushi first calculates the monthly mortgage payment on a median-priced home with a 5% down payment and a mortgage rate of 3% (see chart below): Kushi then takes the monthly cost and subtracts the appreciation the home had over the previous twelve months. The average house price in Dallas increased 17.5% in the second quarter of 2021 compared to last year (this is in line with the national pace). That equates to an equity benefit of approximately $3,550 each month if the pace remains the same (see chart below):

Kushi then takes the monthly cost and subtracts the appreciation the home had over the previous twelve months. The average house price in Dallas increased 17.5% in the second quarter of 2021 compared to last year (this is in line with the national pace). That equates to an equity benefit of approximately $3,550 each month if the pace remains the same (see chart below): We can see the equity gained each month was greater than the monthly mortgage payment, resulting in a negative cost to own. The buyer could build their net worth by $1,830 each month – after paying their mortgage.

We can see the equity gained each month was greater than the monthly mortgage payment, resulting in a negative cost to own. The buyer could build their net worth by $1,830 each month – after paying their mortgage.

Kushi then compares the monthly cost of owning to the cost of renting (see chart below): When adding equity build-up into the equation, the cost of renting is $3,140 more expensive than owning. Again, the First American analysis shows that it’s less expensive to own in each of the top 50 markets in the country when including the equity component.

When adding equity build-up into the equation, the cost of renting is $3,140 more expensive than owning. Again, the First American analysis shows that it’s less expensive to own in each of the top 50 markets in the country when including the equity component.

Bottom Line

If you’re on the fence about whether to buy or rent right now, let’s connect so we can determine if the equity increase in our local market should impact your decision.

Boston real estate for sale search

Ford Realty Inc., Boston Real Estate for Sale

Click to View Google Review

Updated: Boston Real Estate 2021