Boston Condos for Sale and Rent

Home Prices and Mortgage Rates

Boston Condos for Sale Search

Loading...

Home prices increase as falling mortgage rates attract buyers

Home prices nationwide showed the biggest increase in a month while declining mortgage rates are bringing more buyers to the market, according to a new Redfin report.

The median home sale price in the four weeks ended Jan. 15 rose 0.9% from 2022 to $350,250. The jump comes as more potential buyers are conducting home searches and mortgage applications are rising.

More buyers have entered the market in the past four weeks as mortgage rates fell, dropping to 6.15% during the week ended Jan. 19, marking the lowest level since September.

Redfin deputy chief economist Taylor Marr said those who started looking at homes online and scheduling tours at the end of last year are now turning into actual homebuyers.

“Low competition, falling mortgage rates and seller concessions are bringing some buyers back to the market,” Marr said. “That’s helping keep national home prices afloat, which is one bright spot for sellers. But many buyers are still sitting on the sidelines and demand could dip back down if inflation declines slower than expected or mortgage rates rise again.”

Year over year, though, home prices fell in 18 of the country’s 50 most populous metros, during the four weeks ended Jan. 15, the report found.

Prices were down year-over-year 10.1% in San Francisco, 6.7% in San Jose, 5.5% in Austin, 4.3% in Detroit, 3.8% in Seattle, 3.7% in Phoenix, 3.4% in Sacramento, 3.1% in San Diego, 2.8% in Anaheim, California, 2.5% in Chicago, 2.4% in Los Angeles, 2.3% in Oakland, California and 2.2% in Boston.

In Riverside, California, Portland, Oregon, New York, Newark, New Jersey, and Las Vegas, home prices fell less than 2%.

Thirty-year mortgage rates dropped to 6.15% for the week ending Jan. 19. The daily average, according to the report, was 6.04% on Jan. 18. Meanwhile, mortgage applications rose 25% on Jan. 13 from a week prior and purchase applications were down 26% from 2022.

With the lower rate, the average monthly mortgage payment on a median-priced home was $2,262, unchanged from the week prior but down $245 from October’s peak. Year over year, though, monthly mortgage payments are up 30%.

In the four weeks ended Jan. 15, active listings rose 21.8% from last year, marking the biggest annual increase since 2015. Meanwhile, new listings fell 20% from last year, the biggest drop on record.

______________________________________________________________________________________________________________________________________

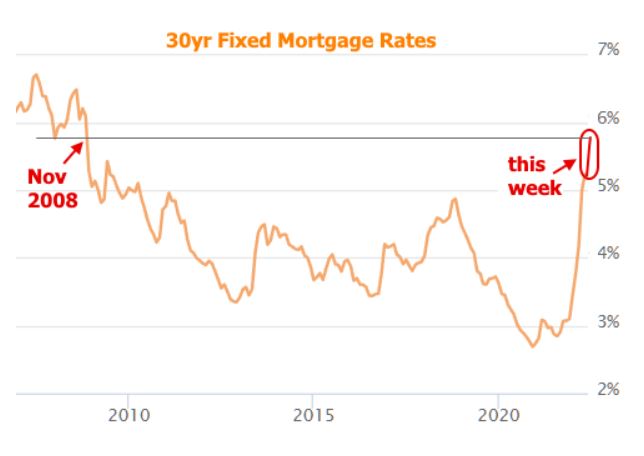

Mortgage Rates Heading for 6%

I picked a great day to start the mortgage-rate tracker in the right-hand column! >>>>

Mortgage rates haven’t been in the 6% range since 2008:

Wondering how to cope? Here are my tips:

- Sellers – Offer to Pay Points. Even if the buyer won’t use your lender, offer to pay 1%-2% of the loan amount to buydown their interest rate. If their lender keeps the money instead of giving a lower rate, well then, heck, at least you tried. But the buyers should appreciate the effort, and two points should reduce the rate by at least 1/4%.

- Sellers – Carry the Financing. If the seller carries all or part of the financing at a reasonable rate, it will help the buyers. Plus, sellers only pay capital-gains taxes on the money you receive, so you’ll get a break there. The big bonus will be if the buyer stops paying – you’ll get your house back too!

- Buyers – Get a Short-Term Mortgage. We call them ARMs, or adjustable-rate mortgages which sounds scary after the neg-am debacle last time. But they offer a fixed-rate for the initial term – just get a seven-year or ten-year loan and refinance once we go into recession and the Feb has to back off again (because they owe $30 trillion themselves, it will probably happen sooner than later).

While the impact on the buyers’ monthly payments is real, it’s the market psychology that will make it worse. Buyers will be expecting lower prices, so instead, consider one of my tips above as an alternative.

Home Prices and Mortgage Rates

____________________________________________________________________________________________________________________________________

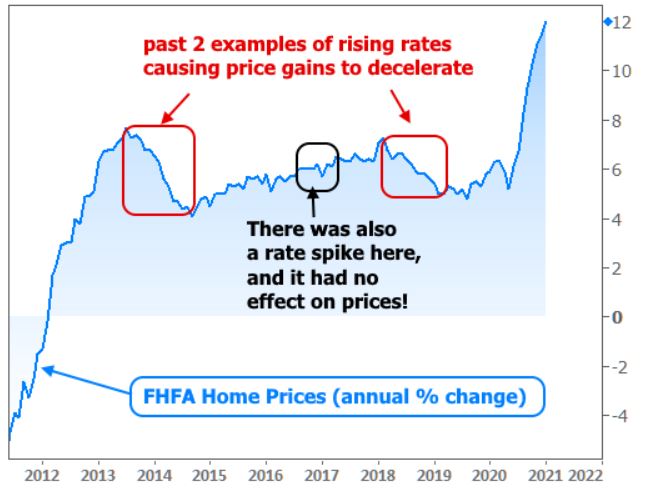

Matthew makes the case here that the current uptick in mortgage rates may not affect home prices:

There was a big rate spike at the end of 2016 that had no discernible effect on prices. This is notable because that rate spike was fueled by economic optimism as opposed to 2013’s rate spike which happened after the Fed said they would begin decreasing their rate-friendly bond buying program. 2018 was somewhat similar as the Fed was continuing to tighten monetary policy and raise short term interest rates.

A case could be made that the current rate spike shares some similarities with 2016. The path of 10yr Treasury yields (a benchmark for longer term rates like mortgages) has largely traced pandemic progress and economic recovery hopes. Yields (aka rates) began rising late last summer as vaccine trials showed promising results and economic data began to improve.

Rates spiked more quickly in the new year as vaccine logistics ramped up and covid-relief legislation was passed. Fiscal spending hurts rates both due to both its positive implications for the economy (a stronger economy supports higher rates) and the implication of more US Treasury issuance (more Treasury supply = lower bond prices = higher bond yields = higher rates).

But it is predicated on mortgage rates staying about where they are today, which is around 3.0% – 3.25%. The demand has been strong enough that rates in the low-3s should be acceptable and that the bidding wars will sort out the rest of what happens to pricing.

He also makes the case that the 10-year bond yield and mortgage rates have re-connected. The 10-year closed at 1.71% yesterday, and if things go right, it will stay in that ballpark.

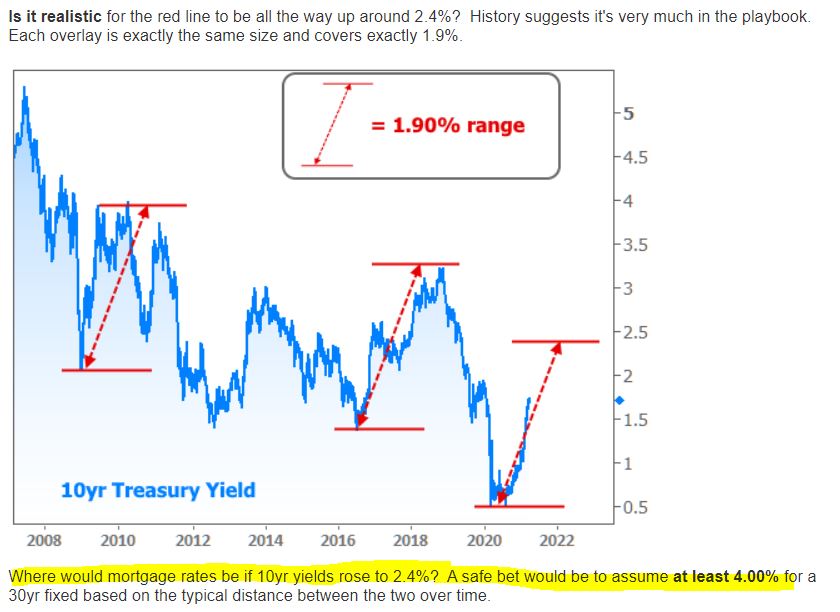

But there has been times when the 10-year has kept rising. If that happens again, we might see 4% rates:

If mortgage rates get back to 4%, we should see pricing flatten out. Let’s keep an eye on the 10-year yield!

Read full article here:

http://www.mortgagenewsdaily.com/consumer_rates/971650.aspx

Why home prices may be pushed higher with low interest rates.

Updated: Boston Real Estate Blog 2022

Click Here to view: Google Ford Realty Inc Reviews