More Foreclosures Coming

Boston Condos for Sale and Apartments for Rent

More Foreclosures Coming

- Total Filings: 367,460 U.S. properties received default notices, scheduled auctions, or bank repossessions.

- Foreclosure Starts: Lenders initiated processes on 289,441 properties, a 14% increase from 2024.

- Bank Repossessions (REOs): Lenders repossessed 46,439 properties, up 27% from 2024.

- Highest Foreclosure Rates: The states with the worst rates in 2025 were Florida (1 in every 230 housing units), Delaware, South Carolina, Illinois, and Nevada.

- Delinquency Dominance: FHA loans represent approximately 38% of active foreclosures and account for 52% of all seriously delinquent loans.

- Economic Strain: FHA borrowers typically have lower income buffers and credit scores (averaging 677), making them more susceptible to rising insurance premiums, property tax reassessments, and inflation.

- New Loss-Mitigation Rules: Experts note that FHA borrowers face heightened risk due to updated loss-mitigation rules that may accelerate timelines for those unable to sustain modified payments.

- Student Loan Impact: Nearly 30% of FHA loan holders have student debt, which has further strained household budgets following the resumption of payments in 2025.

- States with Most Starts: Texas (37,215), Florida (34,336), and California (29,777) led the nation in new foreclosure starts in 2025.

- Metro Areas: MSAs with the highest number of foreclosures starts included New York, Chicago, Houston, Miami, and Los Angeles.

New 2025 report shows foreclosures are on the rise. Learn more with the video below.

More Foreclosures Coming

If you’ve been keeping up with the news lately, you’ve probably come across some articles saying the number of foreclosures in today’s housing market is going up. And that may leave you feeling a bit worried about what’s ahead, especially if you owned a Back Bay during the housing crash in 2008.

The reality is, while increasing, the data shows a foreclosure crisis is not where the market is headed.

Here’s the latest information stacked against the historical data to put your mind at ease.

The Headlines Make the Increase Sound Dramatic – But It’s Not

The increase the media is calling attention to is a little bit misleading. That’s because it’s comparing the most recent numbers to a time when foreclosures were at historic lows. And that lopsided comparison is making it sound like a much bigger deal than it actually is.

Back in 2020 and 2021, there was a moratorium and forbearance program that helped millions of homeowners avoid foreclosure during challenging times. That’s why numbers for just a few years ago were so low.

Now that the moratorium has come to an end, foreclosures are resuming and that means numbers are rising. But it’s an expected increase, not a surprise, and not a cause for alarm. Just because foreclosure filings are up doesn’t mean the housing market is in trouble.

To prove that to you, let’s expand the comparison out a bit more. Specifically, we’ll go all the way back to the housing crash in 2008 – since that’s what people worry may happen again.

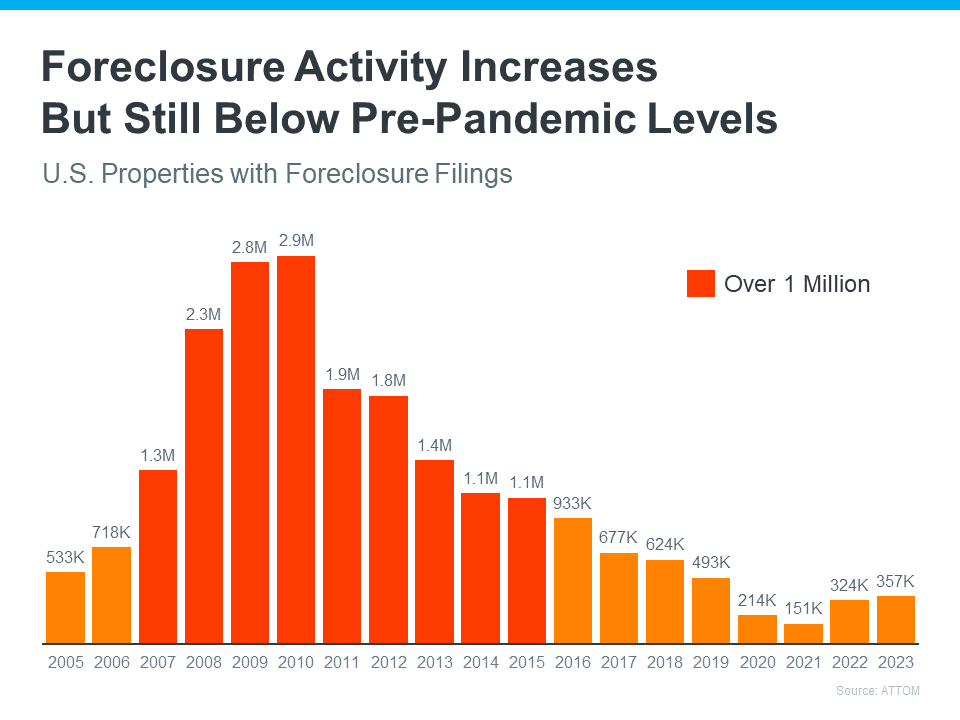

The graph below uses research from ATTOM, a property data provider, to show foreclosure activity has been consistently lower since the crash in 2008:

What the data shows is that things now aren’t anything like they were surrounding the housing crash. The bars in red are when there were over 1 million foreclosure filings a year. In 2023, there were roughly 357,000. That’s a big difference.

A recent article from Bankrate explains one of the reasons things aren’t like they were back then:

“In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes.”

Basically, foreclosure activity is nothing like it was during the crash. That’s because most homeowners today have enough equity to keep them from going into foreclosure. And that’s a really good thing for homeowners and for the market.

The reality is, the data shows a foreclosure crisis is not where the market is today, or where it’s headed.

Boston condos for Sale and the Bottom Line

Right now, putting the data into context is more important than ever. While the housing market is experiencing an expected rise in foreclosures, it’s nowhere near the crisis levels seen when the housing bubble burst, and that won’t lead to a crash in home prices.

*********************************

More Foreclosures Coming

U.S. foreclosures are the highest since the pandemic’s start

by Liz Hughes 2022

January foreclosure filings were the highest since the start of the pandemic, according to a new report.

ATTOM found 23,204 U.S. properties had foreclosure filings last month rising 29% from December and up 139% from a year ago.

Rick Sharga, executive vice president of RealtyTrac said January’s increased level of foreclosure activity wasn’t a surprise as it tends to slow down in November and December before picking up after the start of the new year.

“This year, the increases were probably a little more dramatic than usual since foreclosure restrictions placed on mortgage servicers by the CFPB expired at the end of December,” he said in a press release.

In January lenders repossessed 4,784 properties through the completed foreclosure process, an increase of 57% from December and up 235% from last year. January was the seventh consecutive month of increases.

Six states had at least 100 or more foreclosures with the greatest monthly increase. They included Michigan which was up 622%, Georgia up 163%, Texas with a 98% increase, Tennessee up 50% and Alabama with a 44% increase.

Additionally, five major metros with populations of more than 200,000 had the greatest number of increases. They included Detroit with 1,013, Chicago with 210, New York City at 129, Miami with 113 and Philadelphia with 107.

Nationally, one in every 5,922 homes had a foreclosure filing in January. The highest foreclosure rates in January were in New Jersey (one in every 2,336 housing units), Illinois (one in every 2,740), Nevada (one in every 3,119), Michigan (one in every 3,127) and Ohio which had one in every 3,251.

In areas with populations of at least 200,000, the highest foreclosure rates were in Detroit (one in every 1,547), Atlantic City (one in every 1,564), Cleveland, Ohio, (one in every 1,659), Columbia, South Carolina, (one in every 1,921) and Trenton, New Jersey, (one in every 2,299).

Despite the large increases, Sharga said it’s important to keep these numbers in context.

“Foreclosure completions are still far below normal levels — less than half as many as in January of 2020 before the pandemic was declared, and about 60% lower than the number of foreclosure completions in 2019,” he said. “We’re likely to continue seeing large year-over-year percentage increases for the rest of this year, but it’s also likely that foreclosure activity will remain below historically normal levels until the end of 2022.”

In January foreclosure starts rose in 33 states including the District of Columbia. Lenders began the foreclosure process on 11,854 properties nationally last month, an increase of 29% from December and up 126% from a year prior.

Boston Condos for Sale

More Foreclosures Coming

While the expiration of the federal moratorium on foreclosure filings continues to impact homeowners struggling with the economic effects of the pandemic, the pace of filings has slowed from the initial shock that followed the end of the moratorium on July 31.

According to real estate data provider ATTOM Data Solutions, foreclosure filings, which include default notices, scheduled auctions or bank repossessions, rose 5% in October on a monthly basis and 76% from October 2020, to 20,587 filings.

“As expected, now that the moratorium has been over for three months, foreclosure activity continues to increase,” said Rick Sharga, executive vice president at RealtyTrac, an ATTOM company. “But it’s increasing at a slower rate, and it appears that most of the activity is primarily on vacant and abandoned properties, or loans that were in foreclosure prior to the pandemic.”

Among the 220 U.S. metropolitan statistical areas tracked by ATTOM, Miami and Chicago had some of the highest foreclosure rates, alongside Trenton, N.J., St. Louis and Cleveland. At the state level, Illinois, Florida, New Jersey, Nevada and Ohio had the highest foreclosure rates.

The start of the foreclosure process picked up speed in October nationwide, with a 5% month-over-month increase and a 115% surge from October 2020. New York, Miami, Los Angeles, Houston and Atlanta led the way among major metro areas by foreclosure starts.

“Most foreclosure activity for the next few months is likely to be foreclosure starts, since virtually nothing entered the foreclosure process during the past year,” Sharga said in the release. “The ratio of foreclosure starts to foreclosure completions will normalize over time as we get back to normal levels of activity.”

Foreclosure completions rose 13% month over month and 17% year over year, ATTOM said. Major urban areas with the highest foreclosure completions were St. Louis, Chicago, Baltimore, Philadelphia and New York.

_____________________________________________________________________

_

Boston Condos for Sale

_______________________________________________________________________________________________________________________________________________________________________________________

Colleen M. Sullivan reports in this week’s Banker & Tradesman that almost 70 percent of Bay State homeowners who purchased a home between 2003 and 2007 with some kind of second loan are now underwater.

That translates to about 71,000 homeowners throughout the state who owe more on their homes than they are currently worth. I wonder, how many of those 71,000 homes will go into foreclosure?

File Under: Danger ahead.