Boston Condos for Sale and Rent

Which direction will Boston real estate mortgage rates head in in 2023?

As mortgage rates rose last year, activity in the Boston condo for sale market slowed down. And as a result, condominiums for sale started seeing fewer offers and stayed on the market longer. That meant some homeowners decided to press pause on selling.

Now, however, rates are beginning to come down—and buyers are starting to reenter the market. In fact, the latest data from the Mortgage Bankers Association (MBA) shows mortgage applications increased last week by 7% compared to the week before.

So, if you’ve been planning to sell your house but you’re unsure if there will be anyone to buy it, this shift in the market could be your chance. Here’s what experts are saying about buyers returning to the market as we approach spring.

Mike Fratantoni, SVP and Chief Economist, MBA:

“Mortgage rates are now at their lowest level since September 2022, and about a percentage point below the peak mortgage rate last fall. As we enter the beginning of the spring buying season, lower mortgage rates and more homes on the market will help affordability for first-time homebuyers.”

Lawrence Yun, Chief Economist, National Association of Realtors (NAR):

The upcoming months should see a return of buyers, as mortgage rates appear to have already peaked and have been coming down since mid-November.”

Thomas LaSalvia, Senior Economist, Moody’s Analytics:

“We expect the labor market to remain robust, wages to continue to rise—maybe not at the pace that they did during the pandemic, but that will open up some opportunity for folks to enter homeownership as interest rates stabilize a bit.”

Sam Khater, Chief Economist, Freddie Mac:

“Homebuyers are waiting for rates to decrease more significantly, and when they do, a strong job market and a large demographic tailwind of Millennial renters will provide support to the purchase market.”

Boston Condos for Sale and the Bottom Line

If you’ve been thinking about making a move, now’s the time to get your house ready to sell. Let’s connect so you can learn about buyer demand in our area the best time to put your Boston condo on the market.

__________________________________________________________________________________________________________________________________________________________

(Photo Illustration by The Real Deal with Getty)

Mortgage rates notched their first weekly increase in six weeks just before the new year.

The average rate for a 30-year fixed-rate loan climbed to 6.42 percent from 6.27 percent, according to Freddie Mac data reported by Bloomberg. The figure closes out a year over which mortgage rates more than doubled, pricing out potential homebuyers and locking sellers in place.

As more buyers sit on the sidelines, homes are taking longer to sell. Inventory has risen as a result, but the population of available listings is still down from the pandemic-era housing market.

The number of properties for sale has risen 18 percent since last year, according to a recent report by Redfin, for the biggest gain since 2015. However, the brokerage reported home sales dropped 35.1 percent year-over-year in November — the largest drop since it began tracking sales in 2012.

The buyer of a median-priced home would pay about 60 percent more than last year due to higher borrowing rates, or about $2,100 a month without taxes or insurance, according to Ratiu.

Mortgage rates rose following an increase in 10-year treasury bond yields, which indicated more investors were seeking a safe store for their money. A key inflation metric showed earlier this month that consumers were paying six percent more than a year ago for goods and services.

The Federal Reserve is targeting an annual inflation rate of two percent, suggesting that its campaign to stem high prices and high wages with even higher interest rates is far from over.

_____________________________________________________________________________________________________________________________________

Mortgage rates have been a hot topic in the housing market over the past 12 months. Compared to the beginning of 2022, rates have risen dramatically. Now they’re dropping, and that has to do with everything happening in the economy.

Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), explains it well by saying:

“Mortgage rates dropped even further this week as two main factors affecting today’s mortgage market became more favorable. Inflation continued to ease while the Federal Reserve switched to a smaller interest rate hike. As a result, according to Freddie Mac, the 30-year fixed mortgage rate fell to 6.31% from 6.33% the previous week.”

So, what does that mean for your homeownership plans? As mortgage rates fluctuate, they impact your purchasing power by influencing the cost of buying a home. Even a small dip can help boost your purchasing power. Here’s how it works.

The median-priced home according to the National Association of Realtors (NAR) is $379,100. So, let’s assume you want to buy a $400,000 home. If you’re trying to shop at that price point and keep your monthly payment about $2,500-2,600 or below, here’s how your purchasing power can change as mortgage rates move up or down (see chart below). The red shows payments above that threshold and the green indicates a payment within your target range.

This goes to show, even a small quarter-point change in mortgage rates can impact your monthly mortgage payment. That’s why it’s important to work with a trusted real estate professional who follows what the experts are projecting for mortgage rates for the days, months, and years ahead.

Back Bay Condos and the Bottom Line

Mortgage rates are likely to fluctuate depending on what happens with inflation moving forward, but they have dropped slightly in recent weeks. If a 7% rate was too high for you, it may be time to contact a lender to see if the current rate is more in line with your goal for a monthly housing expense.

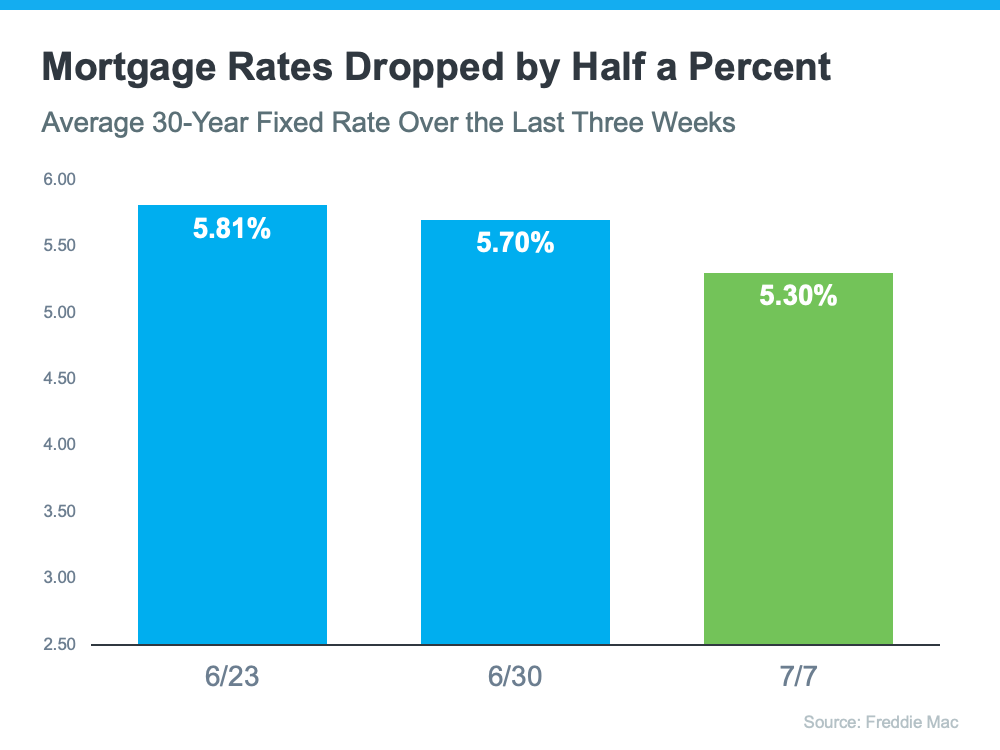

The Drop in Mortgage Rates Brings Good News for Homebuyers

Freddie Mac reports that the average 30-year rate was down to 5.30% from 5.81% two weeks prior (see graph below):

But why is this recent dip such good news for homebuyers? As Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), explains:

“According to Freddie Mac, the 30-year fixed mortgage rate dropped sharply by 40 basis points to 5.3 percent. . . . As a result, home buying is about 5 percent more affordable than a week ago. This translates to about $100 less every month on a mortgage payment.”

That’s because when rates go up (as they have for the majority of this year), they impact how much you’ll pay in your monthly mortgage payment, which directly affects how much you can comfortably afford. The inverse is also true. A decrease in mortgage rates means an increase in your purchasing power.

The chart below shows how a half-point, or even a quarter-point, changes in mortgage rates can impact your monthly payment:

Boston Condos for sale and the Bottom Line

If your home doesn’t meet your needs, this may be the opportunity you’ve been waiting for. Let’s connect to see how you can benefit from the current drop-in mortgage rates.

Updated: Boston Real Estate Blog 2023

Updated: Boston Real Estate Blog 2022

Click to View Google Reviews

Ivy Zelman, CEO of Zelman & Associates, joins Fast Money to discuss interest rates and the impact it could have on the housing market. With CNBC’s Melissa Lee and the Fast Money traders, Guy Adami, Tim Seymour and Bonawyn Eison.

Boston Condos for Sale and Rent

_____________________________________________________________________________________________________________________________

Boston Condo for Sale Search

Boston real estate mortgages

A good article by Matthew on the current rate environment:

Bonds find themselves in an interesting position heading into February.

On the one hand, there’s a well-established tepid recovery narrative that coincides with gradually rising 10yr yields for the past 6 months and, more recently, mortgage rates that begun to take notice. On the other hand, several of the inputs driving those trends are open to criticism, push-back, or other intervening factors that may collectively say “not so fast” to the rising rate trend.

Econ data can bat for either team in this regard and this week brings the month’s biggest reports with ISM PMIs and the big jobs report (NFP). A unified message from the data will likely matter to the bond market, but it might be hard to tell unless those “not so fast” factors are staying silent.

For the sake of clarity, let’s identify these teams.

Team Rising Rates

- Significantly lower Covid case counts (new daily cases are roughly a third of what they were a month ago)

- Vaccine optimism and actual vaccine distribution

- The reopening of economies and re-employment of laid-off workers

- Resilient-to-stronger econ data

- Fiscal stimulus and other sources of excess bond issuance (lots of corporate bonds right now as well)

- Potential progress toward the Fed’s reflationary goals and the eventual inevitability of an attempt to taper asset purchases

Team Not So Fast

- Permanent job destruction – we’re still 10 million jobs short of pre-covid levels and Friday’s forecast calls for only 50k more. At that pace, it takes 16+ years to get those jobs back.

- Vaccine roll-out inefficiencies

- New Covid strain uncertainties

- Political gridlock (decreases Treasury issuance threats)

- Ongoing Fed support implied by lackluster job growth and stubborn reflationary impulses

- The fear of a stock market correction–one that becomes more likely if rates rise too much or too quickly

- General momentum. After all, 10yr yields have been in that linear uptrend for 6 months, making rising rates increasingly susceptible to some technical push-back.

Economic data occupies a very interesting space on both of these teams. Sure, it’s all about covid first and foremost, but covid’s market impact is really all about the economy. In that sense, econ data does more than anything to decide who wins this game.

So why don’t we see bigger reactions to the data? Simply put, even when it comes to significant reports, they’re nothing more than points scored in the middle of a very long, very close game. As long as both teams continue to score, econ data will be hard-pressed to cause a panic in the bond market. But if one team manages to dominate the momentum–i.e. multiple successive econ reports that are much stronger (or weaker) than forecast–rates would likely react accordingly.

Even then, the nature of covid and the current economic reality means that the data could still be questioned if there are current fundamental developments that logically argue that case. For instance, data could be tepid, but if covid case counts are dropping and vaccination rates are ahead of schedule, traders might trade a brighter outlook and simply wait for the econ data to confirm. Conversely, data could be on the up and up, but if something about the covid/vaccine situation deteriorates, traders could disregard near-term economic successes for fear of more lockdowns and unemployment.

http://www.mortgagenewsdaily.com/mortgage_rates/blog/966385.aspx