What Will Happen with Massachusetts Mortgage Rates this Week? Should I lock-in?

Boston Condos for Sale and Apartments for Rent

What Will Happen with Massachusetts Mortgage Rates this Week? Should I lock-in?

What Will Happen with Massachusetts Mortgage Rates this Week? Should I lock-in?

Mortgage and refinance interest rates today, August 8, 2025: It could be a good day to lock in a rate

While mortgage rates have declined this week, rates are not set to drop below the 6% range this year. If you are looking to buy a Boston condo for sale in 2025, this could be a good time to lock in a mortgage while rates are low. Just make sure to choose a mortgage lender with a rate buydown option. With an interest rate buydown program, you can re-lock your interest rate before buying a house if market rates decrease.

- The national average APR for a 30-year fixed mortgage is 6.73%. The average interest rate for a 30-year fixed mortgage is 6.58%, decreasing from last week.

- The national average APR for a 15-year fixed mortgage is 5.94%. The average interest rate for a 15-year fixed mortgage is 5.85%.

- The national average APR for a 30-year fixed refinance is 6.85%.

- Other loan types are also available with varying rates, according to Bankrate.

- What is a rate lock? A mortgage rate lock is a commitment from a lender to offer you a specific interest rate for a set period, typically 30 to 60 days. This protects you if rates rise before you close on your loan.

- When to lock? You can lock in your rate as soon as you complete your loan application and select a mortgage, or you can wait closer to closing, according to CrossCountry Mortgage.

- Benefits of locking: Locking provides peace of mind, ensuring your rate won’t increase before closing.

- Drawbacks of locking: If rates drop after you’ve locked in, you might miss out on a lower rate unless your lender offers a “float-down” option, which usually comes with a fee.

- To lock your rate: You’ll typically need to have your finances reviewed, including credit report, income, assets, and debt-to-income ratio. Your lender will then provide a quote, and if you’re satisfied, you can request to lock the rate.

- Compare quotes: Rates can vary between lenders, so it’s essential to shop around and compare loan estimates from multiple sources.

- Understand fees: Some lenders charge a fee for rate locks, especially for longer lock periods or extensions, according to LendingTree.

- Rate lock expiration: If your rate lock expires before closing, you’ll need to pay a relock or extension fee, and your new rate will be based on current market rates or your original lock, whichever is higher.

Love thy neighbor

Boston Condos for Sale

Click Here to view: Google Ford Realty Inc Reviews

Click to View Google Reviews

Ford Realty Beacon Hill – Condo for Sale Office

Boston condos for sale – Ford Realty Inc

__________________________

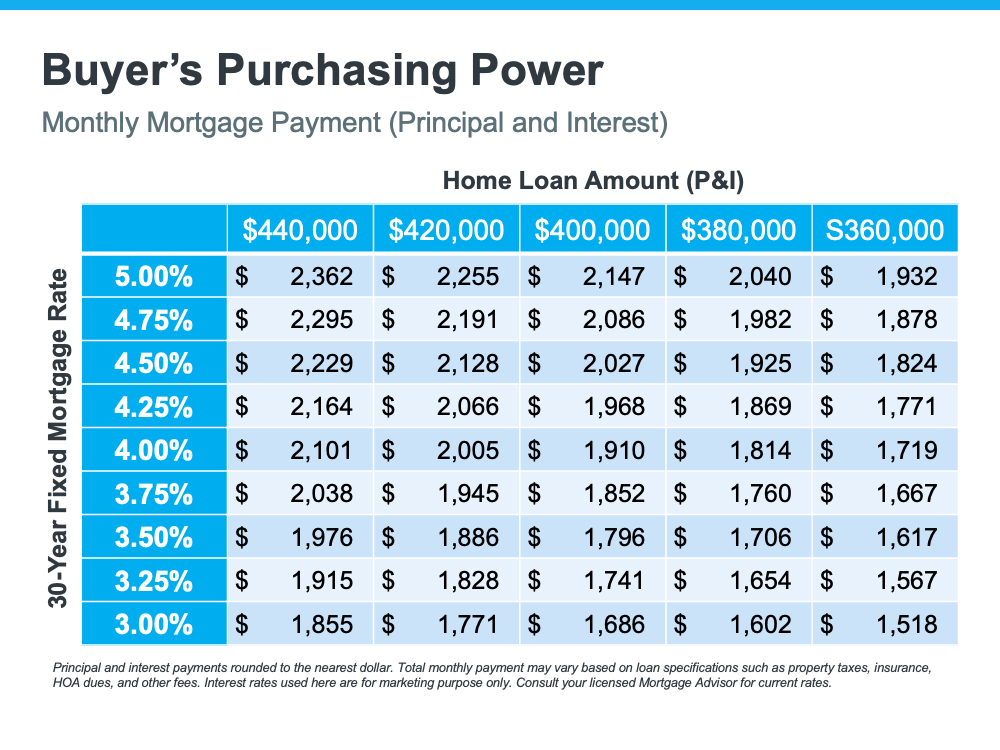

Boston condo mortgage rates have increased significantly since the beginning of the year. Each Thursday, Freddie Mac releases its Primary Mortgage Market Survey. According to the latest survey, the average 30-year fixed-rate mortgage has risen from 3.22% at the start of the year to 3.55% as of last week. This is important to note because any increase in mortgage rates changes what you can afford for a Boston Back Bay condo for sale. To give you an idea of how rising mortgage rates impact your purchasing power, see the table below:

How Can You Know Where Mortgage Rates Are Headed?

While it’s always difficult to know exactly where mortgage rates will go, a great indicator of where they may head is by looking at the 50-year history of the 10-year treasury yield, and then following its path. Understanding the mechanics of the treasury yield isn’t as important as knowing that there’s a correlation between how it moves and how mortgage rates follow. Here’s a graph showing that relationship over the last 50 years:

This correlation has continued into the new year. The treasury yield has started to climb, and that’s driven rates up. As of last Thursday, the treasury yield was 1.81%. That’s 1.74% below the mortgage rate reported the same day (3.55%) and is very close to the average spread we see between the two numbers (average spread is 1.7).

Where Will the Treasury Yield Head in the Future?

With this information in mind, a 10-year treasury-yield forecast would be a good indicator of where mortgage rates may be headed. The Wall Street Journal just surveyed a panel of over 75 academic, business, and financial economists asking them to forecast the treasury yield over the next few years. The consensus was that experts project the treasury yield will climb to 2.84% by the end of 2024. Based on the 50-year history of following this yield, that would likely put mortgage rates at about 4.5% in three years.

While the correlation between the 30-year fixed mortgage rate and the 10-year treasury yield is clear in the data shown above for the past 50 years, it shouldn’t be used as an exact indicator. They’re both hard to forecast, especially in this unprecedented economic time driven by a global pandemic. Yet understanding the relationship can help you get an idea of where rates may be going. It appears, based on the information we have now, that mortgage rates will continue to rise over the next few years. If that’s the case, your best bet may be to purchase a home sooner rather than later, if you’re able.

Boston Condos for Sale and the Bottom Line

Forecasting mortgage rates is very difficult. As Mark Fleming, Chief Economist at First American, once said:

“You know, the fallacy of economic forecasting is don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

However, if you’re either a first-time homebuyer or a current homeowner thinking of moving into a home that better fits your changing needs, understanding what’s happening with the 10-year treasury yield and mortgage rates can help you make an informed decision on the timing of your purchase.

Boston Real Estate Blog Updated 2022

Boston Condos for Sale

Historically low mortgage rates are a big motivator for Boston condo buyers right now. In 2020 alone, rates hit new record-lows 16 times, and the trend continued into the early part of this year. Many hopeful Boston downtown real estate buyers are now wondering if they should put their plans on hold and wait for the lowest rates imaginable. However, the reality is, acting sooner rather than later may be the actual win if you’re ready to buy a Beacon Hill condo for sale

According to Greg McBride, Chief Financial Analyst for Bankrate:

“As vaccines become more widely available and a return to normal starts to come into view, we’ll see mortgage rates bounce off the record lows.”

While only a slight increase in mortgage rates is projected for 2021, some experts believe they will start to rise. Over the past week, for example, the average mortgage rate ticked up slightly, reaching 2.79%. This is still incredibly low compared to the trends we’ve seen over time. According to Freddie Mac:

“Borrowers are smart to take advantage of these low rates now and will certainly benefit as a result.”

You Should lock in now on your Boston Condo. Here’s why.

As mortgage rates rise, the increase impacts the overall cost of purchasing a home. The higher the rate, the higher your monthly mortgage payment, especially as home prices rise too. Sam Khater, Chief Economist at Freddie Mac, says:

“The forces behind the drop in rates have been shifting over the last few months and rates are poised to rise modestly this year. The combination of rising mortgage rates and increasing home prices will accelerate the decline in affordability and further squeeze potential homebuyers during the spring home sales season.”

What does this mean for Boston condo buyers?

Right now, the inventory of houses for sale is also at a historic low, making it more challenging than normal to find a home to buy in many areas. As more buyers hit the market in the typically busy spring buying season, it may become even harder to find a home in the coming months. With this in mind, Len Keifer, Deputy Chief Economist for Freddie Mac, recommends taking advantage of both low mortgage rates and the opportunity to buy:

“If you’ve found a home that fits your needs at a price you can afford, it might be better to act now rather than wait for future rate declines that may never come and a future that likely holds very tight inventory.”

Boston Real Estate and the Bottom Line

While today’s low mortgage rates provide great opportunities for homebuyers, we may not see them stick around forever. If you’re ready to buy a home, let’s connect so you can take advantage of what today’s market has to offer.

Boston Condos for Sale