Boston pre-qualification, pre-approval, and commitment letters in 2025

Boston Real Estate Search

Boston pre-qualification, pre-approval, and commitment letters in 2025

Since the supply of Boston condos for sale is finally growing and mortgage rates are coming down, you may be thinking it’s finally your moment to jump into the market. To make sure you’re ready, you need to get pre-approved for a mortgage.

That’s when a lender looks at your finances, including things like your W-2, tax returns, credit score, and bank statements, to figure out what they’re willing to loan you. After that process, you’ll get a pre-approval letter to show what you can borrow. Here are two reasons why this is essential in today’s market.

Pre-Approval Helps You Know Your Numbers

While home affordability is finally starting to show signs of improving, it’s still tight. So, it’s a good idea to talk to a lender about your loan options and how today’s changing mortgage rates will impact your monthly payment. The pre-approval process is the perfect time for that. In addition to determining the maximum amount you can borrow, pre-approval also helps you understand this piece of the puzzle. As Investopedia says:

“Consulting with a lender and obtaining a pre-approval letter allows you to discuss loan options and budgeting with the lender; this step can clarify your total house-hunting budget and the monthly mortgage payment you can afford.”

You should use this information to tailor your home search to what you’re actually comfortable with budget-wise. Since mortgage rates have inched down some lately, you may find you’re able to afford a bit more than you’d expect for your monthly payment, but you still want to avoid overextending. As CNET explains:

“In many cases, a lender may preapprove you for more than you need to spend on a home. And while it can be tempting to look at houses outside your budget, it won’t help you in the long run. Before you start touring homes, figure out how much you can realistically afford and stick to your budget.”

Pre-Approval Makes Your Offer More Appealing

And once you do find a home you want in your budget, pre-approval has another big perk. It not only makes your offer stronger, it also shows sellers you’ve already undergone a credit and financial check. When a seller sees you as a serious buyer, they may be more attracted to your offer because it seems more likely to go through. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

As mortgage rates trend down, more Boston condo buyers are going to be ready to jump back into the market. And while demand is still limited right now, there’s the potential for competition to pick back up, especially in hot markets. So, why not stack the deck in your favor and make sure you’re putting yourself in the best position possible when you find a home you love?

Boston Condos and the Bottom Line

If you’re planning on buying a home, don’t forget to get pre-approved early in the process. It can help you get a more in-depth understanding of what you can borrow and shows sellers you mean business.

___________

Boston pre-qualification, pre-approval and commitment letters in 2024

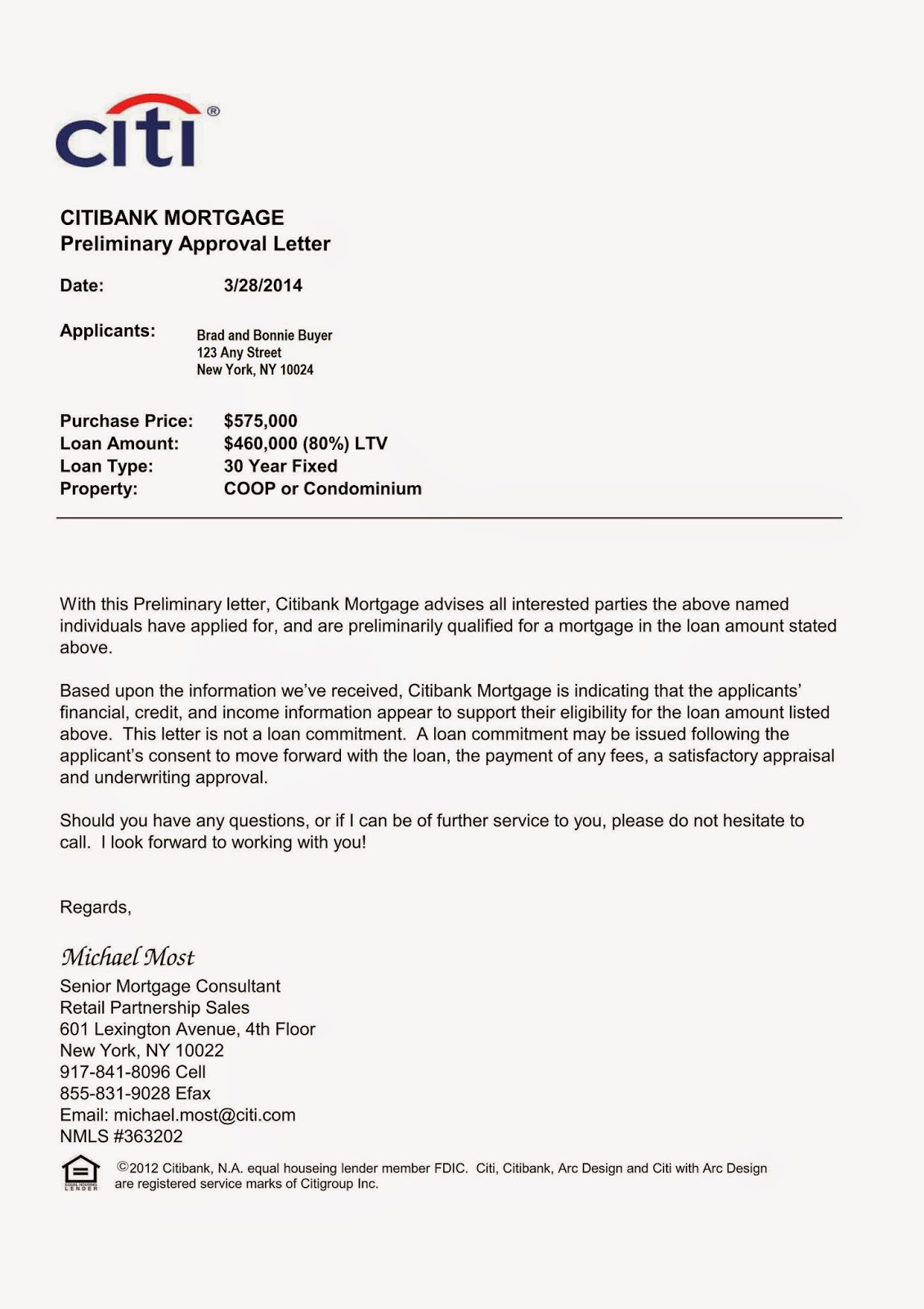

Boston condo loan click to enlarge

One of the most misunderstood terms in Boston real estate is the difference between a “pre-approval” (sometimes referred to as “pre-qualification” or “preliminary loan approval”) and a “loan commitment”. Knowing the differences between the two will help you avoid unpleasant surprises when you are in the process of putting in an offer on a condominium.

I recently spoke with a Boston condo buyer that was interested in a listing he saw on my website. When I asked if he was pre-approved for a condominium loan he told me that he didn’t want to get pre-approved because it would lower his credit score.

I told him that he was overreacting. A credit score may have a temporary hit after several inquiries although an inquiry is not an application for credit. This first-time buyer told me “that’s not what he heard” and that he didn’t want to get a pre-approval every time he viewed a property. I told him one letter is all you need and you don’t need one for each property you view.

Let’s make clear what the difference is between pre-qualification and commitment letters. The pre-qualification letter, informs sellers and their brokers that based upon the information received, the lender is indicating that the applicants’ financial, credit, and income information appear to support them for the loan amount listed on the pre-approval letter. It is not a loan commitment. A loan commitment may be issued following the applicant’s consent to move forward with the loan.

There are three main types of guarantees a bank or mortgage broker will provide, and they each require different up-front evaluations on their part and strength in the market on your part: the pre-qualification, the pre-approval, and underwritten approval. If you’re buying in Beacon Hill, Back Bay, or Boston high-rise condos you’re going to want to know what each of these entails.

Boston Real Estate and the Pre-Qualification Letter

A pre-qualification is just a ballpark figure of how large a mortgage you can afford. For a lender to pre-qualify you, they may ask for your employer’s name and your Social Security number to verify your income and credit score. When a bank prequalifies you, it’s giving you a preliminary statement of how much you could borrow, based on income and asset information you’ve provided. It is not based on any hard evidence, because at this point, you haven’t given your bank statements or had bank officers request your credit report. It’s super basic and is not good for much in the Beacon Hill, Back Bay, or Boston high-rise condo markets, but will help you on what condominiums to start looking at online if you’re just browsing.

Boston Real Estate and the Pre-Approval Letter

A bank will issue a mortgage pre-approval once it has all your documents in hand. These could include income verification from employers, recent tax returns, bank and brokerage statements, and credit reports. That assessment will result in a pre-approval letter from the lender that you can present when you bid for a home. Having a pre-approval in hand gives you a jump on other potential buyers. It lets the seller know you’re a good candidate, and that the bank is likely to award you a loan. It’ll also make you feel more prepared to buy. This is the most common document provided to buyers by lenders. Keep in mind that you’re not required to borrow from the bank that issues your pre-qualification or pre-approval.

Boston Condos and Mortgage Commitment Letters

A loan commitment requires verification of your ability to pay the mortgage (real estate loan). This process includes such items as your income, employment history, assets, and credit score. It also requires the review of the Boston condo itself, such as the value and condition of the property, the status of title to the property, and a property appraisal to list just a few items.

The next question, many Boston condo buyers ask: Do most pre-approvals result in loan commitments? Assuming the lender is diligent during the pre-approval process, yes. However, it is not uncommon for a consumer to receive a pre-approval and then find out later that the pre-approval was subject to conditions the consumer could not meet, thus prohibiting them from receiving the loan, or forcing them to accept a loan at a higher interest rate or lower loan amount.

If you’d like more information please feel free to contact Ford Realty at 617-595-3712.

From Wikipedia, the free encyclopedia

In lending, pre-approval has two meanings:

“The first is that a lender, via public or proprietary information, feels that a potential borrower is completely creditworthy enough for a certain credit product, and approaches the potential customer with a guarantee that should they want that product, they would be guaranteed to get it. This rarely happens in the financial services industry, and when it does happen, it is usually loaded with fine print that is not immediately disclosed. Usually, what happens is pre-qualification, instead.

Although, to a typical consumer, “you’re pre-approved” means “you already passed the approval process and therefore are guaranteed to be immediately granted the loan if you apply,” the literal meaning is different. The literal meaning is “at a stage before approval.” Thus, pre-approved creates no obligation whatsoever on the lender and no rights whatsoever to the potential borrower. “Pre-approved” is thus a popular advertising catchphrase to induce people to apply for a loan.

The second meaning relates to mortgage lending. People interested in buying a house can often approach a lender, who will check their credit history and verify their income, and they can provide assurances they would be able to get a loan up to a certain amount. This pre-approval can then help a buyer find a home that is within their loan amount range. Buyers can ask for a letter of pre-approval from the lender, and when shopping for a home can have possibly an advantage over others because they can show the seller that they are more likely to be able to buy the house. Often real estate agents prefer to work with a buyer who has a pre-approval as it demonstrates that they are well-qualified to receive financing and are serious about buying a home. A pre-approval is based on the documentation the borrower supplies at the time of application, and any actual eligibility to receive the pre-approved loan depends on the terms and conditions of the pre-approval and ability to secure the loan before the pre-approval expires.

Boston Real Estate Blog Updated 2022

You may have heard that it’s important to get pre-approved for a mortgage at the beginning of the homebuying process, but what does that really mean, and why is it so important? Especially in today’s market, with rising home prices and high Boston condo for sale buyer competition, it’s crucial to have a pre-approval letter prior to making an offer. Here’s why.

Boston Condo for Sale Market

Being intentional and competitive are musts when buying a home this year. Pre-approval from a lender is the only way to know your true price range and how much money you can borrow for your loan. Just as important, being able to present a pre-approval letter shows sellers you’re a qualified buyer, something that can really help you land your dream home in an ultra-competitive market.

With limited housing inventory, there are many more buyers active in the market than there are sellers, and that’s creating some serious competition. According to the National Association of Realtors (NAR), homes today are receiving an average of 3.8 offers for sellers to consider. As a result, bidding wars are still common. Pre-approval gives you an advantage if you get into a multiple-offer scenario, and these days, it’s likely you will. When a seller knows you’re qualified to buy the home, you’re in a better position to potentially win the bidding war.

Freddie Mac explains:

“By having a pre-approval letter from your lender, you’re telling the seller that you’re a serious buyer, and you’ve been pre-approved for a mortgage by your lender for a specific dollar amount. In a true bidding war, your offer will likely get dropped if you don’t already have one.”

Every step you can take to gain an advantage as a buyer is crucial when today’s market is constantly changing. Interest rates are rising, prices are going up, and lending institutions are regularly updating their standards. You’re going to need guidance to navigate these waters, so it’s important to have a team of professionals such as a loan officer and a trusted real estate advisor making sure you take the right steps and can show your qualifications as a buyer when you find a home to purchase.

Boston condos and the Bottom Line

In a competitive market with low inventory, a pre-approval letter is a game-changing piece of the homebuying process. Not only does being pre-approved bring clarity to your homebuying budget, but it shows sellers how serious you are about purchasing a home

Back to Boston condos for sale homepage

Contact me to find out more about Boston condos for sale or any property.

SEARCH FOR CONDOS FOR SALE AND RENTALS

For more information please contact one of our on-call agents at 617-595-3712.

Update Boston Real Estate updated in 2025

Beacon Hill condos for sale

- Tips on buying a Beacon Hill condo

- Boston Beacon Hill condo buyers how to beat all-cash offers

- 5 tips on buying a Beacon Hill condo for sale

- Benefits of buying a Beacon Hill condo

- Design tips for Beacon Hill condo buyers

- Boston Beacon Hill condos for sale 5 must-know terms

- The difference between a Beacon Hill condo and a Beacon Hill loft

- Common mistakes when buying a Beacon Hill condo

- Buying a Beacon Hill condo with kids

- Is it time to ditch my Beacon Hill condo agent?

- Beacon Hill condos for sale: Do I need 20% down?

- 3 signs you’re going to buy a Boston Beacon Hill condo

- 6 principles to know when buying a Beacon Hill condo

- How to select a Boston Beacon Hill condo agent

- Boston Beacon Hill condos for sale down payment

- Boston Beacon Hill condos finance

- Beacon Hill condos for sale what is negotiable

- Beacon Hill condos for sale: What it takes to get a mortgage.

- Boston Beacon Hill condos for sale. Understand the condo association

- How much do Boston Beacon Hill condos cost?

Boston condos for sale near Downtown/Midtown Boston

Back Bay Boston condos

Beacon Hill Boston condos

Charlestown Boston condos

Navy Yard Charlestown Boston condos

Dorchester Boston condos

Fenway Boston condos

Jamaica Plain Boston condos

Leather District Boston condos

Midtown Boston condos

Seaport District Boston condos

South Boston new condos

South End new condos

Waterfront new condos

North End new condos

West End new condos

East Boston condosCondos around the Midtown area to rent:

Back Bay area condos for rent

Beacon Hill area condos for rent

Charlestown area condos for rent

Navy Yard Charlestown area condos for rent

Dorchester area condos for rent

Fenway area condos for rent

Jamaica Plain area condos for rent

Leather District area condos for rent

Midtown area condos for rent

Seaport District area condos for rent

South Boston area condos for rent

South End area condos for rent

Waterfront area condos for rent

North End area condos for rent

West End area condos for rent

East Boston area condos for rentClick here: Boston Midtown Condos For Sale.